RBS 2013 Annual Report Download - page 424

Download and view the complete annual report

Please find page 424 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

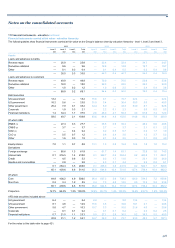

Notes on the consolidated accounts

422

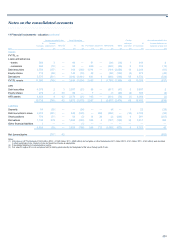

11 Financial instruments - valuation continued

Valuation techniques

The table below shows a breakdown of valuation techniques and the ranges for those unobservable inputs used in valuation models and techniques that

have a material impact on the valuation of Level 3 financial instruments. The table excludes unobservable inputs where the impact on valuation is less

significant. Movements in the underlying input may have a favourable or unfavourable impact on the valuation depending on the particular terms of the

contract and the exposure. For example an increase in the credit spread of a bond would be favourable for the issuer and unfavourable for the note

holder. Whilst we indicate where we consider that there are significant relationships between the inputs, these inter-relationships will be affected by

macro economic factors including interest rates, foreign exchange rates or equity index levels.

Level 3 (£bn) Range

Financial instruments

A

ssets Liabilities Valuation technique Unobservable inputs Lo

w

High

Loans 0.5 0.2 Price based Price (2) 80% 100%

Discounted cash flow model (DCF) Credit spreads (3) 0bps 831bps

Recovery rates (4) 10% 67%

Yield (2) 8% 24%

Probability of default (5) 5% 20%

Deposits 0.1 Option pricing Volatility (6) 27% 30%

Debt securities

RMBS 0.3 Price based Price (2) 0% 96%

DCF Probability of default (5) 2% 7%

Conditional prepayment rates (CPR) (7) 0% 7%

Yield (2) 6% 19%

CDO and CLO 1.1 Price based Price (2) 0% 100%

DCF Yield (2) 10% 29%

Probability of default (5) 2% 11%

Other ABS 0.3 Price based Price (2) 0% 100%

Other debt securities 0.4 DCF Credit spreads (3) 99bps 140bps

Price based Price (2) 68% 100%

Equity securities 0.7 Price based Price (2) 69% 158%

EBITDA multiple EBITDA multiple (8) 1x 40x

DCF Yield 47% 64%

Recovery rates (4) 0% 40%

Derivatives

Foreign exchange 1.3 0.7 DCF Correlation (9) (55%) 100%

Option pricing model Volatility (6) 6% 26%

Interest rate 1.4 0.6 Option pricing model Correlation (9) (55%) 100%

DCF CPR (7) 2% 20%

Equities and commodities 0.8 Option pricing model Volatility (6) 16% 40%

Credit 0.8 0.9 Price based Price (2) 0% 100%

DCF based on defaults and recoveries Recovery rates (4) 0% 100%

Upfront points (10) 2% 100%

Credit spreads (3) 35bps 725bps

For the notes to this table refer to the following page.