RBS 2013 Annual Report Download - page 312

Download and view the complete annual report

Please find page 312 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

310

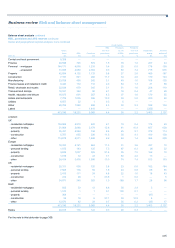

Balance sheet analysis continued

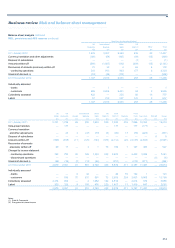

REIL, provisions and AFS reserves continued

Provisions and AFS reserves methodology

The Group's consumer portfolios, which consist of high volume, small

value credits, have highly efficient largely automated processes for

identifying problem credits and very short timescales, typically three

months, before resolution or adoption of various recovery methods.

Corporate portfolios consist of higher value, lower volume credits, which

tend to be structured to meet individual customer requirements.

Provisions are assessed on a case by case basis by experienced

specialists with input from professional valuers and accountants. The

Group operates a transparent provisions governance framework, setting

thresholds to trigger enhanced oversight and challenge.

Analyses of provisions are set out on pages 312 to 314.

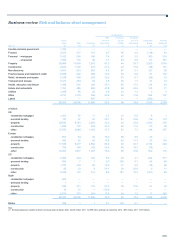

Available-for-sale financial assets are initially recognised at fair value plus

directly related transaction costs and are subsequently measured at fair

value with changes in fair value reported in owners’ equity until disposal,

at which stage the cumulative gain or loss is recognised in profit or loss.

When there is objective evidence that an available-for-sale financial asset

is impaired, any decline in its fair value below original cost is removed

from equity and recognised in profit or loss.

The Group reviews its portfolios of available-for-sale financial assets for

evidence of impairment, which includes: default or delinquency in interest

or principal payments; significant financial difficulty of the issuer or

obligor; and it becoming probable that the issuer will enter bankruptcy or

other financial reorganisation. However, the disappearance of an active

market because an entity’s financial instruments are no longer publicly

traded is not evidence of impairment. Furthermore, a downgrade of an

entity’s credit rating is not, of itself, evidence of impairment, although it

may be evidence of impairment when considered with other available

information. A decline in the fair value of a financial asset below its cost

or amortised cost is not necessarily evidence of impairment. Determining

whether objective evidence of impairment exists requires the exercise of

management judgement. The unrecognised losses on the Group’s

available-for-sale debt securities are concentrated in its portfolios of

mortgage-backed securities. The losses reflect the widening of credit

spreads as a result of the reduced market liquidity in these securities and

the current uncertain macroeconomic outlook in the US and Europe. The

underlying securities remain unimpaired.

Analyses of AFS debt securities and related AFS reserves are set out on

page 316 and 317.

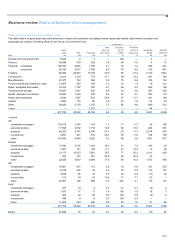

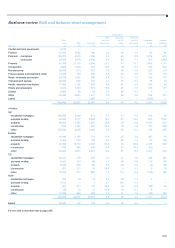

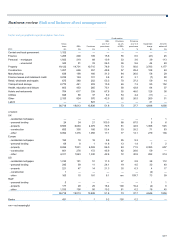

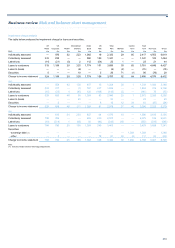

REIL flow statement

REIL are stated without giving effect to any security held that could reduce the eventual loss should it occur or to any provisions marked.

UK UK International Ulster US Retail & Central

Retail Corporate Wealth Banking Bank Commercial Markets items Core Non-Core Total

£m £m £m £m £m £m £m £m £m £m £m

A

t 1 January 2013 4,569 5,452 248 422 7,533 1,146 396 — 19,766 21,374 41,140

Currency translation and other

adjustments — 11 2 (11) 134 (21) 1 — 116 279 395

Disposal of subsidiaries — — — — — — — — — (89) (89)

A

dditions 1,302 4,825 132 431 2,479 282 14 1 9,466 3,397 12,863

Transfers (1) (445) 418 — 133 — — — — 106 (1) 105

Transfers to performing book — (54) (3) (118) — — — — (175) (108) (283)

Repayments (1,045) (3,654) (87) (106) (1,403) (89) (27) — (6,411) (3,982) (10,393)

A

mounts written-off (815) (772) (15) (281) (277) (284) (46) — (2,490) (1,856) (4,346)

A

t 31 December 2013 3,566 6,226 277 470 8,466 1,034 338 1 20,378 19,014 39,392

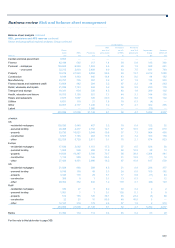

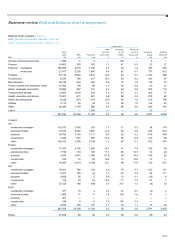

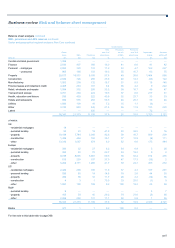

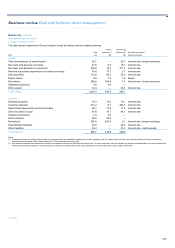

Non-Core (by donating divisions)

UK International Ulster US Retail &

Corporate Banking Bank Commercial Other Total

£m £m £m £m £m £m

A

t 1 January 2013 2,622 6,907 11,399 418 28 21,374

Currency translation and other adjustments 8 67 206 (2) — 279

Disposal of subsidiaries — — (89) — — (89)

A

dditions 1,327 1,283 705 80 2 3,397

Transfers (1) (1) — — — — (1)

Transfers to performing book (4) (101) (2) — (1) (108)

Repayments (1,350) (1,774) (816) (41) (1) (3,982)

A

mounts written-off (379) (875) (431) (165) (6) (1,856)

A

t 31 December 2013 2,223 5,507 10,972 290 22 19,014

Note:

(1) Represents transfers between REIL and potential problem loans.