RBS 2013 Annual Report Download - page 245

Download and view the complete annual report

Please find page 245 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

243

When the relationship is transferred, GRG conducts a detailed

assessment of the viability of the business as well as the ability of

management to deal with the causes of financial difficulty. Following

GRG’s initial file assessment and, if appropriate, wider due diligence with

input from independent experts (sector experts, accountants and

surveyors), various options are presented to the customer. A strategy is

then agreed with the customer for dealing with the distressed loan.

The objective is to find a mutually acceptable solution, including

repayment, refinancing or transfer to another bank if that is the

customer’s preferred option. Once a solution is found, management of

the loans may be transferred back to the performing divisions. If the

business is not viable and a turnaround is not possible, insolvency may

be an option.

Wholesale forbearance

Definition

Forbearance takes place when a concession is made on the contractual

terms of a loan in response to a customer’s financial difficulties.

Concessions granted where there is no evidence of financial difficulty, or

where any changes to terms and conditions are within the Group’s usual

risk appetite (for a customer new to the Group), or reflect improving credit

market conditions for the customer, are not considered forbearance.

A number of options are available to the Group. Such actions are tailored

to the customer’s individual circumstances. The aim of such actions is to

restore the customer to financial health and to minimise risk to the Group.

To ensure that forbearance is appropriate for the needs and financial

profile of the customer, the Group applies minimum standards when

assessing, recording, monitoring and reporting forbearance.

Types of wholesale forbearance

Wholesale forbearance may involve the following types of concessions:

• Payment concessions and loan rescheduling, including extensions

in contractual maturity, may be granted to improve the customer’s

liquidity. Concessions may also be granted on the expectation that

the customer’s liquidity will recover when market conditions improve.

In addition, they may be granted if the customer will benefit from

access to alternative sources of liquidity, such as an issue of equity

capital. These options are commonly used in commercial real estate

transactions, particularly where a shortage of market liquidity rules

out immediate refinancing and makes short-term collateral sales

unattractive.

• Debt may be forgiven, or exchanged for equity, where the

customer’s business or economic environment means that it cannot

meet obligations and where other forms of forbearance are unlikely

to succeed. Debt forgiveness is commonly used for stressed

leveraged finance transactions. These are typically structured on the

basis of projected cash flows from operational activities, rather than

underlying tangible asset values. Provided that the underlying

business model, strategy and debt level are viable, maintaining the

business as a going concern is the preferred option, rather than

realising the value of the underlying assets.

A temporary covenant waiver, a recalibration of covenants or a covenant

amendment may be used to cure a potential or actual covenant breach.

In return for this relief, the Group would seek to obtain a return

commensurate with the risk that it is required to take. The increased

return for the increased risk can be structured flexibly to take into account

the customer’s circumstances, for example increased margin on a cash

or payment in kind basis, and/or deferred return instruments.

The contractual margin may be amended to bolster the customer’s day-

to-day liquidity to help sustain the customer’s business as a going

concern. This would normally be a short-term solution. As set out above,

the Group would seek to obtain a return commensurate to the risk that it

is required to take and this can be structured in the same ways set out

above.

Loans may be forborne more than once, generally where a temporary

concession has been granted and circumstances warrant another

temporary or permanent revision of the loan’s terms. All customers are

assigned a PD and related facilities a LGD. These are re-assessed prior

to finalising any forbearance arrangement in light of the loan’s amended

terms. Where forbearance is no longer viable, the Group will consider

other options such as the enforcement of security and/or insolvency

proceedings.

The ultimate outcome of a forbearance strategy is unknown at the time of

execution. It is highly dependent on the cooperation of the borrower and

the continued existence of a viable business. The following are generally

considered to be options of last resort:

• Enforcement of security or otherwise taking control of assets -

Where the Group holds collateral or other security interest and is

entitled to enforce its rights, it may enforce its security or otherwise

take ownership or control of the assets. The Group’s preferred

strategy is to consider other possible options prior to exercising

these rights.

• Insolvency - Where there is no suitable forbearance option or the

business is no longer regarded as sustainable, insolvency will be

considered. Insolvency may be the only option that ensures that the

assets of the business are properly and efficiently distributed to

relevant creditors.

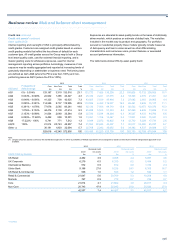

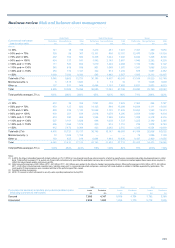

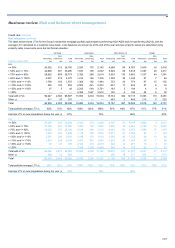

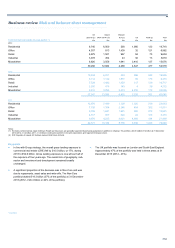

The data presented in the tables below include loans forborne during

2011, 2012 and 2013 which individually exceeded thresholds set at

divisional level. The Group continues to refine its reporting processes for

forborne loans and, as a result, in 2013, thresholds were reduced to

range from nil to £3 million. During 2011 and 2012, these thresholds

ranged from nil to £10 million. The proportion of the Watch and GRG

population covered by these thresholds has changed over time as the

thresholds have been reduced. In 2013, this was 90% (2012 - 84%).

As part of the Group’s ongoing review of forbearance reporting, the

amounts shown as “Completed forbearance” relating to 2012 and 2013

now include loans granted covenant concessions only. These were

disclosed by way of a note in 2012. While the Group considers these

types of concessions qualitatively different from other forms of

forbearance, they constitute a significant proportion of wholesale

forbearance and were therefore included.