RBS 2013 Annual Report Download - page 261

Download and view the complete annual report

Please find page 261 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

259

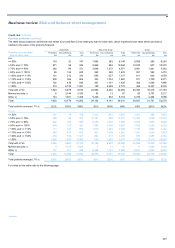

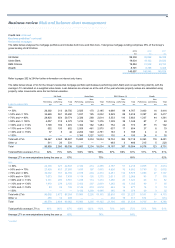

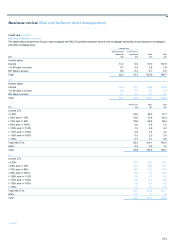

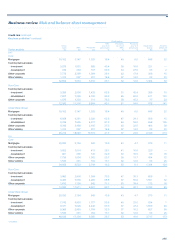

UK Retail Ulster Bank RBS Citizens (1)

Non- Non- Non-

Performing performing Total Performing performing Total Performing performing Total

Loan-to-value ratio £m £m £m £m £m £m £m £m £m

2011

<= 50% 21,537 285 21,822 2,568 222 2,790 4,745 49 4,794

> 50% and <= 70% 25,598 390 25,988 1,877 157 2,034 4,713 78 4,791

> 70% and <= 90% 33,738 671 34,409 2,280 223 2,503 6,893 125 7,018

> 90% and <= 100% 7,365 343 7,708 1,377 128 1,505 2,352 66 2,418

> 100% and <= 110% 3,817 276 4,093 1,462 130 1,592 1,517 53 1,570

> 110% and <= 130% 1,514 199 1,713 2,752 322 3,074 1,536 53 1,589

> 130% and <= 150% 60 15 75 2,607 369 2,976 626 28 654

> 150% — — — 2,798 748 3,546 588 27 615

Total with LTVs 93,629 2,179 95,808 17,721 2,299 20,020 22,970 479 23,449

Other (2) 567 13 580 — — — 681 23 704

Total 94,196 2,192 96,388 17,721 2,299 20,020 23,651 502 24,153

Total portfolio average LTV (3) 67% 80% 67% 104% 125% 106% 76% 91% 77%

A

verage LTV on new originations during the year (3) 63% 74% 63%

Notes:

(1) Includes residential mortgages and home equity loans and lines (refer to page 260 for a breakdown of balances).

(2) Where no indexed LTV is held.

(3) Average LTV weighted by value is calculated using the LTV on each individual mortgage and applying a weighting based on the value of each mortgage.

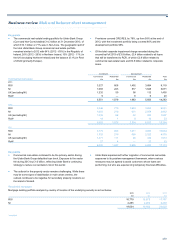

Key points

UK Retail

• The UK Retail mortgage portfolio was £99.3 billion at 31 December

2013, an increase of 0.3% from 31 December 2012. The mortgages

included £9.1 billion (2012 - £7.9 billion) of residential buy-to-let

lending.

• As at 31 December 2013, approximately 43% of the portfolio

consisted of fixed rate, 5% a combination of fixed and variable rates

and the remainder were variable rate mortgages (including those on

managed rates). The interest only proportion of the total portfolio

was 26%.

• Gross new mortgage lending amounted to £14.4 billion and the

average LTV by volume was 62.7% compared to 61.3% at

31 December 2012. The average LTV calculated by weighted LTV

of lending was 66.6% (2012 - 65.2%).

• Based on the Halifax Price Index at September 2013, the portfolio-

average indexed LTV by volume was 54.1% (2012 - 58.1%) and

62.0% by weighted value of debt outstanding (2012 - 66.8%). The

ratio of total outstanding balances to total indexed property

valuations was 45.1% (2012 - 48.5%).

*unaudited

• All new mortgage business is subject to a comprehensive

assessment. This includes: i) an affordability test which includes a

stressed interest rate that is higher than the customer pay rate; ii)

credit scoring; iii) a maximum loan-to-value of 90% with the

exception of the UK Government backed schemes Help-to-Buy

(from the fourth quarter of 2013), New Buy and My New Home

products where lending of up to 95% is provided; and iv) a range of

policy rules that restrict the availability of credit to borrowers with

higher risk characteristics, for example highly indebted and/or

adverse payment behaviour on previous borrowings.

• The arrears rate (defined as more than three payments in arrears,

excluding repossessions and shortfalls post property sale), fell to

1.3% (2012 - 1.5%). The number of properties repossessed in 2013

was 1,532 compared with 1,426 in 2012. Arrears rates remained

sensitive to economic developments and benefited from the low

interest rate environment.

• The impairment charge for mortgage loans was £30 million for 2013

compared to £92 million in 2012, reflecting a lower level of defaults

and reduced loss rates as valuations improved on properties held as

security on defaulted debt.