RBS 2013 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

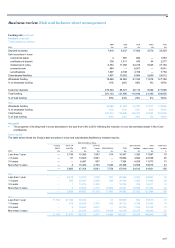

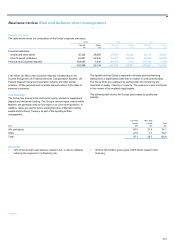

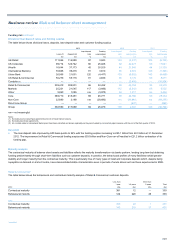

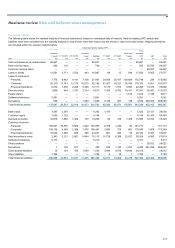

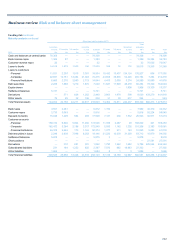

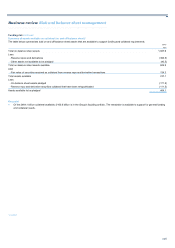

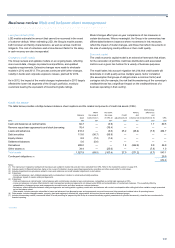

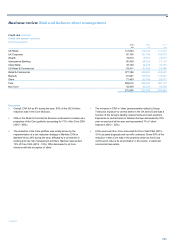

Business review Risk and balance sheet management

228

Credit risk

Definition

Credit risk is the risk of financial loss due to the failure of a customer or

counterparty to meet its obligation to settle outstanding amounts.

Sources of credit risk

The Group is exposed to credit risk as a result of a wide range of

business activities. The most significant source of credit risk is lending.

The second most significant source is counterparty credit risk, which

results from the Group’s activities in the derivatives and securities

financing transaction markets.

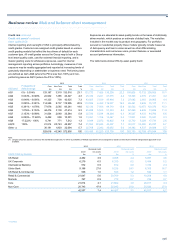

The Group offers a number of lending products where it has an

irrevocable obligation to provide credit facilities to a customer. Security

may be obtained to mitigate the risk of loss in the form of physical

collateral, such as commercial real estate assets and residential property,

or financial collateral such as cash or bonds. Also included in the Group’s

lending are exposures arising from leasing activities.

Derivatives and securities financing transactions expose the Group to

counterparty credit risk, which is the risk of loss arising from a failure of a

customer to meet obligations which vary in value by reference to a

market factor.

The Group holds debt securities with the intention of selling them and so

is exposed to market risk. However, it also holds some debt securities

generally for liquidity management purposes, and is exposed to credit risk

as a result.

The Group is exposed to credit risk from off-balance sheet products such

as trade finance activities and guarantees.

Credit risk governance

A strong credit risk management function is vital to support the ongoing

profitability of the Group. The potential for loss is mitigated through a

robust credit risk culture in the business units and through a focus on

sustainable lending practices. The Group’s credit risk management

function is responsible for credit approval and managing concentration

risk, as well as credit risk control frameworks and acts as the ultimate

authority for the approval of credit. This, together with strong independent

oversight and challenge, enables the business to maintain a sound credit

environment.

The Group Chief Credit Officer (GCCO), through the Group Credit Risk

(GCR) function, is responsible for the development of, and ensuring

compliance with, Group-wide policies and credit risk frameworks as well

as Group-wide assessment of provision adequacy. The risk management

functions, located in the Group’s business divisions, are responsible for

the execution of these policies.

The divisional credit risk management functions work together with GCR

to ensure that the risk appetite set by the Group Board is met. The credit

risk function in each division is managed by a Chief Credit Officer, who

reports jointly to a divisional Chief Risk Officer and to the GCCO.

Divisional credit risk management activities include transaction analysis,

credit approval, ongoing credit risk stewardship, and early problem

identification and management.

The Executive Risk Forum (ERF) considers and approves material

aspects of the Group’s credit risk management framework, such as credit

risk appetite and limits for portfolios of strategic significance. The ERF

has delegated approval authority to the Group Credit Risk Committee, a

functional sub-committee of the Group Risk Committee, to act on credit

risk matters. These include, but are not limited to, credit risk appetite and

limits (within the overall risk appetite set by the Board and the ERF),

credit risk strategy and frameworks, credit risk policy and the oversight of

the credit profile across the Group. There are separate Group Credit Risk

Committees for the retail and wholesale portfolios and these are chaired

by the GCCO.

The Group Audit Committee (GAC) provides oversight of the Group’s

provision adequacy. The GCCO is accountable to the GAC for the

adequacy of the Group’s provisions, both individual and collective.

The Group Provisions Committee, which is chaired by either the Group

Chief Risk Officer or the GCCO, approves recommendations from the

divisional provisions committees.

Key trends in the credit risk profile of the Group, performance against

limits and emerging risks are set out in the RBS Risk Management

Monthly Report provided to the Executive Committee, the Board Risk

Committee and the Group Board.

Risk appetite and concentration framework

Risk appetite is set using specific quantitative targets under stress,

including earnings volatility and capital adequacy. The Group’s credit risk

framework has therefore been designed around the factors that influence

the Group’s ability to meet those targets. These include product and

asset class, industry sector, single name and country concentrations. Any

of these factors could generate higher earnings volatility under stress

and, if not adequately controlled, could undermine capital adequacy.

Tools such as stress testing and economic capital are used to measure

credit risk volatility and develop links between Group risk appetite targets

and the credit risk control framework. The frameworks are supported by a

suite of Group-wide and divisional policies that set out the risk

parameters within which divisions must operate. The Group also

manages its exposures to counterparty credit risk closely, using portfolio

limits and specific tools to control more volatile or capital intensive

business areas.

Wholesale

Four formal frameworks are used to manage wholesale credit

concentration risk. The Group continually reassesses its frameworks to

ensure that they remain appropriate for its varied business franchises and

current economic conditions, as well as to reflect further refinements in

the Group’s risk measurement models.