RBS 2013 Annual Report Download - page 253

Download and view the complete annual report

Please find page 253 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

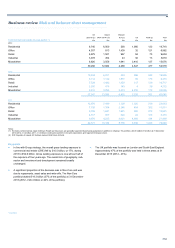

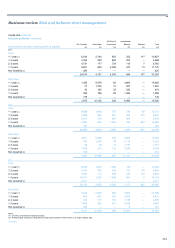

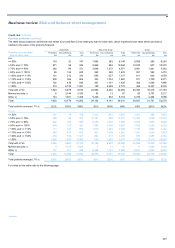

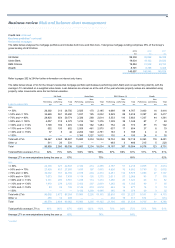

Business review Risk and balance sheet management

251

Impact of forbearance on provisioning

Wholesale

Forbearance may result in the value of the outstanding debt exceeding

the present value of the estimated future cash flows. This may result in

the recognition of an impairment loss or a write-off.

Provisions for forborne wholesale loans are assessed in accordance with

the Group’s normal provisioning policies (refer to Group impairment loss

provisioning on page 250). The customer’s financial position and

prospects as well as the likely effect of the forbearance, including any

concessions granted, are considered in order to establish whether an

impairment provision is required. Individual impairment assessments for

wholesale loans are reassessed in the light of any revisions to the loan's

terms.

All wholesale customers are assigned a PD and related facilities an LGD.

These are re-assessed prior to finalising any forbearance arrangement in

light of the loan’s amended terms and any revised grading incorporated in

the calculation of the impairment loss provisions for the Group’s

wholesale exposures.

For performing counterparties, credit metrics are an integral part of the

latent provision methodology and therefore the impact of covenant

concessions will be reflected in the latent provision. For non-performing

loans, covenant concessions will be considered in the overall provision

adequacy for these loans.

In the case of non-performing loans that are forborne, the loan

impairment provision assessment almost invariably takes place prior to

forbearance being granted. The quantum of the loan impairment

provision may change once the terms of the forbearance are known,

resulting in an additional provision charge or a release of the provision in

the period the forbearance is granted.

The transfer of wholesale loans subject to forbearance from impaired to

performing status follows assessment by relationship managers in GRG.

When no further losses are anticipated and the customer is expected to

meet the loan’s revised terms, any provision is written-off and the balance

of the loan returned to performing status.

Retail

Provisions are assessed in accordance with the Group’s provisioning

policies (refer to Group impairment loss provisioning on page 250).

Impairment provisions in respect of loans subject to forbearance are

evaluated as follows:

In UK Retail performing loans are subject to a latent loss provision but

form a separate risk pool for 24 months. The higher of the observed

default rates and PDs are used in the latent provisioning calculations for

these loans to ensure that appropriate provision is held. Furthermore, for

these portfolios the latent provision incorporates extended emergence

periods. Once such loans are no longer separately identified, the use of

account level PDs refreshed monthly in the latent provision methodology

captures the underlying credit risk without a material time lag.

There is no reassessment of the PD at the time forbearance is granted

but the loan will be the subject to the latent provisioning methodology

described above. Non-performing loans are subject to a collectively

assessed provision methodology.

In Ulster Bank performing loans are subject to a latent loss provision but

form a separate risk pool for the period of forbearance. The performance

of forbearance arrangements is analysed and breakage (a single missed

payment) rates computed. The higher of the breakage rate and the

modelled PD for this separate risk pool is used when calculating the

latent provision. Furthermore, for this portfolio the latent provision

incorporates an extended emergence period. Once such loans are no

longer separately identified, the use of account level PDs refreshed

monthly in the latent provision methodology captures the underlying

credit risk without a material time lag. There is no reassessment of the

PD at the time forbearance is granted but the loan will be the subject to

the latent provisioning methodology described above. Non-performing

loans are subject to a collectively assessed provision methodology.

However, loans not 90 days past due that are subject to forbearance

arrangements involving a reduction in contractually required cash flows

i.e. the forgiveness of interest and where arrears have not been

capitalised are classified as non-performing. They form a separate risk

pool for the period of forbearance and the related loan loss provision is

computed using Ulster Bank’s latent loss provision methodology.

Non-performing loans are grouped into homogeneous portfolios sharing

similar credit characteristics according to the asset type. Further

characteristics such as LTVs, arrears status and default vintage are also

considered when assessing recoverable amount and calculating the

related provision requirement. While non-performing forbearance retail

loans do not form a separate risk pool, the LGD models used to calculate

the collective impairment provision are affected by agreements made

under forbearance arrangements.

In RBS Citizens, retail loans subject to forbearance are segmented from

the rest of the non-forborne population and assessed individually for

impairment loss throughout their lives until the loans are repaid or fully

written off. The amount of recorded impairment depends on whether the

loan is collateral dependent. If the loans are considered collateral

dependent, the excess of the loan’s carrying amount over the fair value of

the collateral is the impairment amount. If the loan is not deemed

collateral dependent, the excess of the loans’ carrying amount over the

present value of expected future cash flows is the impairment amount.

Any confirmed losses are charged off immediately.

Write-offs

The Group normally writes-off loans when it has exhausted all its

collection strategies and has no realistic chance of recovering the money

it is owed. Refer to pages 382 and 383 for further information on the

Group’s write-off policies and practices.