RBS 2013 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

It has been noted before that when economies

are emerging from recessions rooted in high

levels of debt and stresses in the financial

system, growth is slower than in the typical

recovery. That was the experience again

in 2013 in the major markets in which RBS

operates.

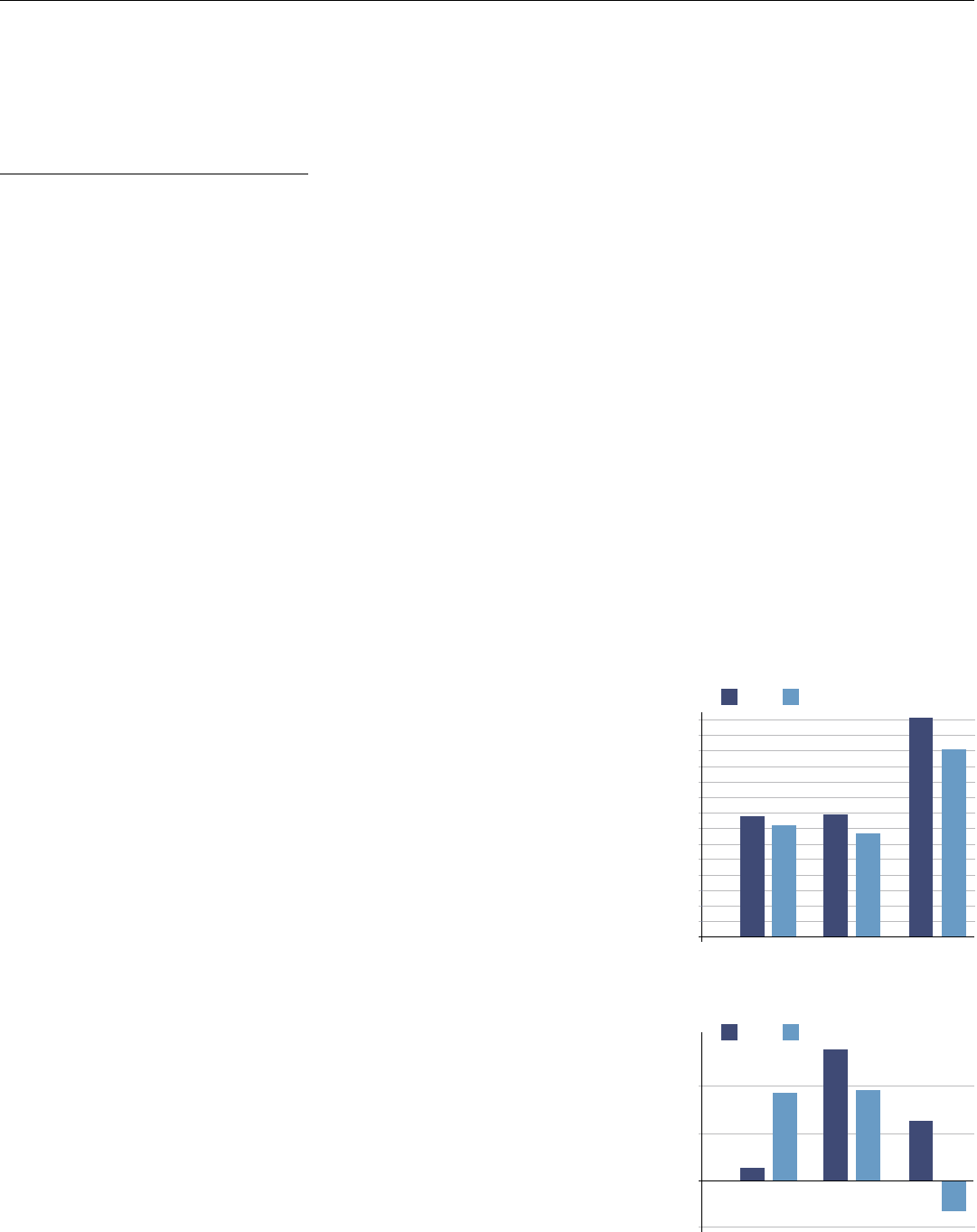

In the UK, performance improved. Total

economic activity, as measured by gross

domestic product (GDP), grew by 1.9%

compared with growth of 0.3% in 2012. At the

start of the year, expectations had been for an

increase of only 1.0%. Consumption led the

way, despite falling real wages. There were

more people in work and households drew

down savings to fund spending.

Unemployment fell, from around 7.9% at the

start of the year towards 7.0% at its end.

Housing market activity accelerated sharply,

prompted in part by measures to encourage

house purchases such as Help to Buy.

According to the Halifax house price index,

the average price of a house in the UK

increased by 5.8% during the year. Other

indices reported stronger price growth.

Prices look to have risen in all parts of the UK

but inflation was strongest in London, where

prices rose by more than 10%.

Inflation ended the year at the 2.0% target

having averaged 2.6% for the year as a

whole. The Bank of England continued its

ultra-loose monetary policy stance. The Bank

Rate remained at 0.5%, although market

rates increased towards the end of the year

on expectations of tighter monetary policy in

the United States. There were no additions

to the stock of assets purchased through the

quantitative easing programme. In August

2013, the Monetary Policy Committee began

offering ‘forward guidance’ on its intentions.

It said that it will not consider changing the

Bank Rate or the stock of assets purchased

until the unemployment rate reaches 7.0%,

unless inflation threatens to take off or there

are concerns about financial stability.

The Funding for Lending Scheme was

adjusted during the course of the year to

enhance the incentives for banks to lend

to small firms and later to withdraw that

support for lending to individuals. The Bank of

England’s Credit Conditions Survey suggested

that the supply of credit had expanded

towards the end of the year.

In the face of considerable fiscal austerity and

continuing disputes about the public finances,

which led to a government shutdown in the

autumn, GDP growth in the United States was

1.9% compared with 2.8% in 2012. There was

encouraging news on the job market, where

unemployment had fallen to 6.7% in December

2013, although part of the fall was accounted

for by people leaving the job market rather

than finding work. The housing market again

performed strongly, with prices up 14% in the

year to November.

In December, the Federal Reserve took the

first formal steps towards tightening monetary

policy. It announced that it would reduce

the amount of assets purchased under its

quantitative easing programme by $10 billion

each month, with the programme likely

to be ended in the second half of 2014. It

maintained its guidance that the Fed Funds

Target Rate would remain at 0.25% until the

unemployment rate reaches 6.5%.

Ireland was able in early 2014 to exit the

adjustment programme it had agreed with

the European Central Bank, the European

Commission and the International Monetary

Fund. However, GDP contracted by 0.7%

in the four quarters to Q3 2013. The export

sector continued to benefit from the boost

to competitiveness delivered by falling real

wages, although export performance also

reflected the decision of companies with

limited local activity to domicile in Ireland.

For Ireland, gross national product (GNP) is a

better measure of the performance of Ireland’s

domestic economy and people’s material

well-being. It reflects the income residents

receive rather than the value of the incomes

generated in the country, an important

distinction where there is a large foreign-

owned sector that remits profits overseas.

GNP increased by 2.7%.

Unemployment averaged 13.2% and finished

the year at 12.4%. House prices rose by 6.4%,

the first year-on-year increase since 2007.

However, rises were confined to Dublin, where

prices increased by 16%. Outside the capital,

prices fell slightly. Nationally, prices ended the

year 45% below their 2007 level.

Entering 2013, the greatest economic concern

was how problems related to sovereign debt

in the euro zone would be managed. With the

exception of Cyprus, there were none of the

episodes of concern that had marked previous

years. Markets were generally convinced that

the European Central Bank would indeed ‘do

what it takes’ to sustain the single currency.

Further steps were taken towards a banking

union. Nevertheless, the region’s economy

remained weak. Unemployment averaged

12.1%, a record, and inflation fell to 0.8% at

the end of the year.

Economic

and monetary

environment

28 Economic and monetary environment

Unemployment rates, % December

Real GDP growth rates, %

UK US RoI

0%

3%

2%

1%

-1%

UK US RoI

14

12

10

8

6

4

2

0

2012 2013

2012 2013