RBS 2013 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

216

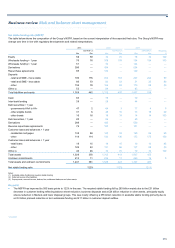

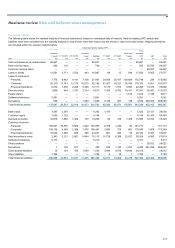

Funding risk

Funding sources

The Group’s primary funding source is its customer deposit base,

primarily built through its retail and commercial franchises in the UK,

Ireland and the US. These deposits form a stable base which fully funds

the Group’s customer lending activities.

Complementary to its deposit funding, the Group also accesses various

wholesale markets for funding, on both a public and private basis. These

include long-term secured and unsecured debt, short-term money

markets and repurchase agreements. The Group has set policies for the

prudent use of wholesale funding, as part of its wider liquidity policies.

Maintaining access to global capital markets provides the Group’s

funding base with diversity. Over time the Group’s wholesale funding mix

has been diversified by currency, geography, maturity and type. The

Group accesses the wholesale funding markets directly or through its

main operating subsidiaries via established funding programmes. The

use of different entities to access the market from time to time allows the

Group to further diversify its funding mix and in certain limited

circumstances demonstrate to regulators that specific operating

subsidiaries enjoy market access in their own right.

The Group may access various funding facilities offered by central banks

from time to time. The use of such facilities can be both part of a wider

strategic objective to support initiatives to help stimulate economic growth

or as part of the Group’s broader liquidity management and funding

strategy. Overall usage and repayment of available central bank facilities

will fit within the Group’s overall liquidity risk appetite and concentration

limits.

During 2013, the Group repaid €8.5 billion of the original €10 billion

borrowed under the European Central Bank’s Long Term Refinancing

Operation. The remaining balance is used to fund certain of the Group’s

Eurozone banking subsidiaries and the usage of this facility will be

evaluated on an ongoing basis. The Group has not drawn down any

additional funds under the Bank of England’s Funding for Lending

Scheme during the year and has repaid the initial drawing of £750 million

in order to manage its excess cash position. The Group remains

committed to supporting the objectives of the Funding for Lending

scheme.

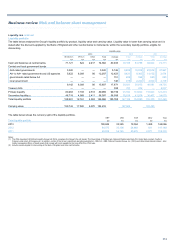

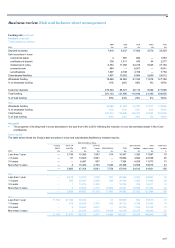

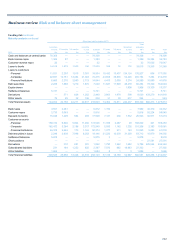

Analysis

Funding sources

The Group’s balance sheet composition is a function of the broad array of

product offerings and diverse markets served by its core divisions. The

structural composition of the balance sheet is augmented as needed

through active management of both asset and liability portfolios. The

objective of these activities is to optimise the liquidity profile in the normal

business environment, while ensuring adequate coverage of all cash

requirements under extreme stress conditions.

As set out below the Group’s asset and liability types broadly match.

Customer deposits provide more funding than customer loans absorb;

repurchase agreements are largely covered by reverse repurchase

agreements; interbank lending and funding largely match each other and

this gap has narrowed over the past five years; and derivative assets are

largely matched against derivative liabilities.

The table below shows the Group’s sources and uses of funding.

2013

Liabilities Assets

£bn £bn

Customer deposits (1) 407 373 Customer loans and advances (1)

Bank deposits (short-term only) (1) 14 18 Loan and advances to banks (1)

Trading liabilities (2) 67 93 Trading assets (2)

Other liabilities and equity (3) 100 90 Other assets (3)

Repurchase agreements 85 76 Reverse repurchase agreements

Term wholesale funding (1) 69 90 Primary liquidity portfolio

Funded balance sheet 742 740 Funded balance sheet

Derivatives 286 288 Derivatives

1,028 1,028

Notes:

(1) Excludes held for trading.

(2) Financial instruments classified as held-for-trading (HFT) excluding security financing transactions and derivatives.

(3) Includes non-HFT financial instruments and non-financial assets/liabilities.