RBS 2013 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

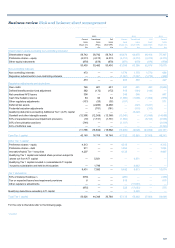

Business review Risk and balance sheet management

199

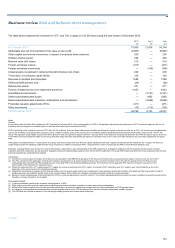

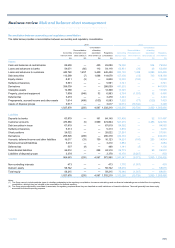

The table below analyses the movement in CET1 and Tier 2 capital on a FLB3 basis during the year ended 31 December 2013.

CET1 Tier 2 Total

£m £m £m

A

t 1 January 2013 37,908 12,876 50,784

A

ttributable loss net of movements in fair value of own credit (8,887) — (8,887)

Share capital and reserve movements in respect of employee share schemes 200 — 200

Ordinary shares issued 264 — 264

Nominal value of B shares 510 — 510

Foreign exchange reserve (217) — (217)

Foreign exchange movements — (106) (106)

A

ctuarial gains recognised in retirement benefit schemes (net of tax) 200 — 200

Termination of contingent capital facility 320 — 320

Decrease in goodwill and intangibles 1,588 — 1,588

Defined benefit pension fund (28) — (28)

Deferred tax assets 971 — 971

Excess of expected loss over impairment provisions 4,423 — 4,423

Grandfathered instruments — (3,121) (3,121)

Dated subordinated debt issues — 1,862 1,862

Dated subordinated debt maturities, redemptions and amortisation — (2,666) (2,666)

Prudential valuation adjustments (PVA) (471) — (471)

Other movements (13) (112) (125)

A

t 31 December 2013 36,768 8,733 45,501

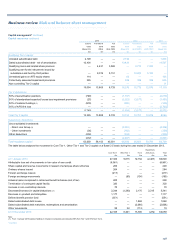

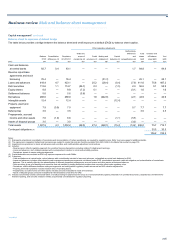

Notes:

General:

In accordance with the PRA’s Policy Statement PS7/13 issued in December 2013 on the implementation of CRD IV, all regulatory adjustments and deductions to CET1 have been applied in full (i.e. no

transition) with the exception of unrealised gains on AFS securities which will be included from 2015.

CRD IV and Basel III will impose a minimum CET1 ratio of 4.5% of RWAs. There are three buffers which will affect the Group: the capital conservation buffer set at 2.5%; the counter-cyclical capital buffer

(up to 2.5% of RWAs), to be applied when macroeconomic conditions indicate areas of the economy are over-heating; and the Global-Systemically Important Bank buffer currently set at 1.5% for the

Group. The regulatory target capital requirements will be phased in and are expected to apply in full from 1 January 2019, in the meantime using national discretion the PRA can apply a top-up. As set out

in the PRA’s Supervisory Statement SS3/13, the Group and other major UK banks and building societies are required to meet a CET1 ratio of 7% after taking into account certain adjustments set by the

PRA.

PRA guidance indicates that from 1 January 2015, the Group must meet at least 56% of its Pillar 2A capital requirement with CET1 capital and the balance with Additional Tier 1 capital. The Pillar 2A

capital requirement is the additional capital that the Group must hold, in addition to meeting its Pillar 1 requirements in order to comply with the PRA’s overall financial adequacy rule.

Estimates, including RWAs, are based on the current interpretation, expectations, and understanding of the CRR requirements, anticipated compliance with all necessary enhancements to model

calibration and other refinements, as well as further regulatory clarity and implementation guidance from the UK and EU authorities. The actual CRR impact may differ from these estimates when the final

technical standards are interpreted and adopted.

Capital base:

(1) Includes the nominal value of B shares (£0.5 billion) on the assumption that RBS will be privatised in the future and that they will count as permanent equity in some form by the end of 2017.

(2) The PVA, arising from the application of the prudent valuation requirements to all assets measured at fair value, has been included in full in line with the guidance from the PRA and uses

methodology discussed with the PRA pending the issue of the final RTS by the European Banking Authority. The full amount of the applicable PVA has been included in provisions in the

determination of the deduction for expected losses.

(3) Where the deductions from AT1 capital exceed AT1 capital, the excess is deducted from CET1 capital. The excess of AT1 deductions over AT1 capital in year one of transition is due to the

application of the current rules to the transitional amounts.

(4) Insignificant investments in equities of other financial entities (net): long cash equity positions are considered to have matched maturity with synthetic short positions if the long position is held for

hedging purposes and sufficient liquidity exists in the relevant market. All the trades are managed and monitored together within the equities business.

(5) Based on current interpretations of the final draft of the RTS on credit risk adjustments, issued in July 2013, the Group’s standardised latent provision has been reclassified to specific provision and is

therefore no longer included in Tier 2 capital.

Risk-weighted assets:

(1) Current securitisation positions are shown as risk-weighted at 1,250%.

(2) RWA uplifts include the impact of credit valuation adjustments and asset valuation correlation on banks and central counterparties.

(3) RWAs reflect implementation of the full internal model method suite, and include methodology changes that took effect immediately on CRR implementation.

(4) Non-financial counterparties and sovereigns that meet the eligibility criteria under CRR are exempt from the credit valuation adjustments volatility charges.

(5) The CRR final text includes a reduction in the risk-weight relating to small and medium-sized enterprises.

*unaudited