RBS 2013 Annual Report Download - page 267

Download and view the complete annual report

Please find page 267 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

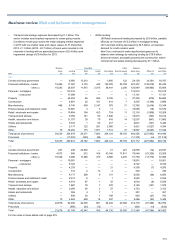

Business review Risk and balance sheet management

265

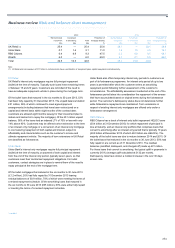

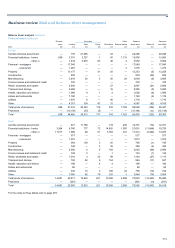

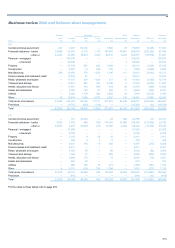

Ulster Bank Group (Core and Non-Core)

Overview

At 31 December 2013, Ulster Bank Group accounted for 10% of the

Group’s total gross loans to customers (2012 and 2011 - 10%) and 8% of

the Group’s Core gross loans to customers (2012 and 2011 - 8%) Ulster

Bank’s financial performance continued to be impacted by the

challenging economic climate in Ireland, with impairments remaining

elevated in the wholesale bank as a result of limited liquidity in the

economy which continues to depress the property market and domestic

spending. Additionally, in the fourth quarter of 2013 the Group announced

a recovery strategy for loans transferring to RCR. This resulted in a

significant increase in provisions as the move from a through the cycle

strategy to a 3 year deleverage, reduced expected realisations.

The impairment charge of £4,793 million for 2013 (2012 - £2,340 million;

2011 - £3,717 million) was driven by a combination of new defaulting

customers and higher provisions on existing defaulted cases due

primarily to the above mentioned RCR strategy. Provisions as a

percentage of risk elements in lending increased to 76% in 2013, from

57% in 2012, predominantly as a result of this change in strategy,

combined with the deterioration in the value of the Non-Core commercial

real estate development portfolio.

Core

The impairment charge for the year of £1,774 million (2012 - £1,364

million; 2011 - £1,384 million) reflected the difficult economic climate in

Ireland, and most particularly the RCR deleverage strategy across the

corporate portfolios. The mortgage portfolio improved notably in 2013,

accounting for £235 million (13%) of the total 2013 impairment charge

(2012 - £646 million; 2011 - £570 million) due to lower debt flows driven

by improved collections performance and stabilising residential property

prices.

Non-Core

The impairment charge for the year was £3,019 million (2012 - £976

million; 2011 - £2,333 million), with the commercial real estate sector

accounting for £2,674 million (89%) of the total 2013 impairment charge,

again reflecting the RCR strategy.

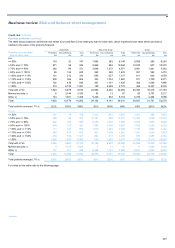

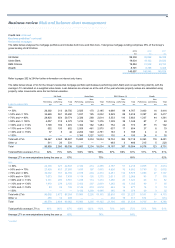

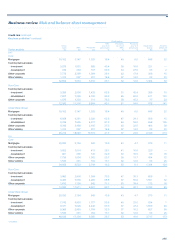

The table below analyses Ulster Bank Group’s loans, REIL, impairments

and related credit metrics by sector.

Credit metrics

REIL Provisions Provisions

Gross as a % of as a % of as a % of Impairment Amounts

loans REIL Provisions gross loans REIL gross loans charge (1) written-off

Sector analysis £m £m £m % % % £m £m

2013

Core

Mortgages 19,034 3,235 1,725 17.0 53 9.1 235 34

Commercial real estate

- investment 3,419 2,288 1,151 66.9 50 33.7 593 51

- development 718 472 331 65.7 70 46.1 153 4

Other corporate 7,039 2,277 1,984 32.3 87 28.2 771 149

Other lending 1,236 194 187 15.7 96 15.1 22 39

31,446 8,466 5,378 26.9 64 17.1 1,774 277

Non-Core

Commercial real estate

- investment 3,211 3,006 2,162 93.6 72 67.3 837 53

- development 6,915 6,757 6,158 97.7 91 89.1 1,837 370

Other corporate 1,479 1,209 1,069 81.7 88 72.3 345 6

11,605 10,972 9,389 94.5 86 80.9 3,019 429

Ulster Bank Group

Mortgages 19,034 3,235 1,725 17.0 53 9.1 235 34

Commercial real estate

- investment 6,630 5,294 3,313 79.8 63 50.0 1,430 104

- development 7,633 7,229 6,489 94.7 90 85.0 1,990 374

Other corporate 8,518 3,486 3,053 40.9 88 35.8 1,116 155

Other lending 1,236 194 187 15.7 96 15.1 22 39

43,051 19,438 14,767 45.2 76 34.3 4,793 706

Note:

(1) Of which £3.2 billion was due to RCR and the related change of strategy.

*unaudited