RBS 2013 Annual Report Download - page 329

Download and view the complete annual report

Please find page 329 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

327

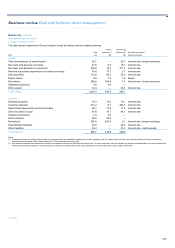

VaR back-testing*

The table below shows regulatory back-testing exceptions for a period of 250 days for 1-day 99% traded regulatory VaR vs. Clean and Hypo P&L for the

legal entities approved by the PRA and De Nederlandsche Bank.

Back-testing exceptions Model

Description Clean Hypo status

The Royal Bank of Scotland plc — — Green

National Westminster Bank Plc 1 1 Green

RBS Securities Inc — — Green

RBS Financial Products Inc — — Green

The Royal Bank of Scotland N.V. 1 1 Green

Key points

• Statistically the Group would expect to see back-testing exceptions

1% of the time over a one-year period. From a capital requirement

perspective, the PRA categorises a firm’s VaR model as green,

amber or red. A green model status is consistent with a satisfactory

VaR model and is achieved for models that have four or fewer

exceptions in a continuous 12 month period. The Group’s VaR

model has maintained a green status for its regulated legal entities

and hence has considered that no action is required to rectify or

adapt its VaR models.

• The exception at the NatWest level was mainly driven by a large

move in inflation following an Office of National Statistics

announcement in January that it would not be changing the RPI

calculation.

• The exception at the RBS NV level was primarily a result of a

significant rise in Indian bond yields as the country’s central bank

unexpectedly raised benchmark interest rates by 200 basis points.

The table below shows internal back-testing exceptions for a period of 250 days for 1-day 99% traded internal VaR vs. Clean and Hypo P&L for

major Markets businesses.

Back-testing exceptions

Description Clean Hypo

A

sset Backed Products — —

Treasury Markets — —

Emerging Markets — —

Equities — —

Currency Options 1 1

Interest Rate Options North America — —

Non Linear Trading 2 2

Delta Flow (flow rates) 1 1

CEM Funding (derivative funding risk) — —

Flow Credit — —

Currencies — 6

Key points

• As mentioned above, statistically the Group would expect to see

back-testing exceptions 1% of the time over a one-year period.

At Group level, there were no exceptions during 2013,

confirming that the model was satisfactory.

• The businesses presented in the table above are subject to quarterly

governance by the PRA. For some of these businesses, exceptions

were noted during 2013 and analysis conducted as explained below.

*unaudited

• The exceptions in Currency Options, Non-Linear Trading and Delta

Flow occurred in the normal course of business and were mainly

related to volatile currencies and rates following a Bank of England

announcement on interest rates, a US Federal Reserve

announcement regarding tapering of its quantitative easing

programme and a statistical release indicating slow growth in

the Chinese economy.

• The exceptions in Currencies were mainly due to currency

fluctuations, driven primarily by increased volatility in the Australian

dollar, Singapore dollar and Japanese yen. Investigation into the

number of exceptions confirmed that the VaR model used for this

business was satisfactory.