RBS 2013 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

113

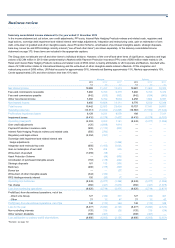

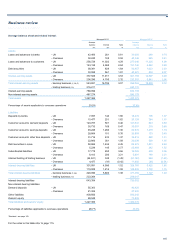

Tax

The tax charge for 2013 was £382 million (2012 - £441 million).

Loss per share

Basic loss per ordinary and equivalent B share from continuing

operations was 81.3p per share compared with 54.5p per share in 2012.

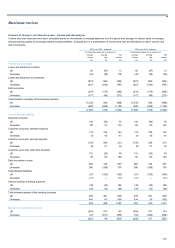

2012 compared with 2011 - managed

Operating profit

Group operating profit, was £2,952 million compared with £1,141 million

in 2011. The improvement was driven by lower costs in Markets,

reflecting reduced headcount and lower levels of variable compensation,

and a better operating performance in Non-Core, where losses fell by

32%. These improvements were partially offset by weaker performance in

Retail & Commercial, as economic conditions remained difficult.

Total income

Total income declined by 6% to £22,085 million, primarily reflecting lower

net interest income.

Net interest income

Group net interest income declined by 7% to £11,417 million largely

reflecting lower interest-earning asset balances. Group net interest

margin (NIM) increased slightly, despite very low interest rates and strong

deposit competition.

Non-interest income

Non-interest income decreased by £443 million in 2012 principally driven

by lower net fees and commissions and a fall in insurance net premium

income. Net fees and commissions fell largely due to weaker consumer

spending volumes in the UK together with legislation changes in the US.

Operating expenses

Total operating expenses fell by 7% to £13,854 million, with staff costs

down 6% as headcount fell by 8,300 to 119,200. The decline in expenses

was largely driven by Non-Core run-down and lower variable

compensation (particularly in Markets), including variable compensation

award reductions and clawbacks following the settlements reached with

UK and US authorities in relation to attempts to manipulate LIBOR. The

run-off of discontinued businesses in Markets and International Banking,

following the restructuring announced in January 2012, and simplification

of processes and headcount reduction in UK Retail also yielded cost

benefits. Group cost: income ratio was flat at 63%.

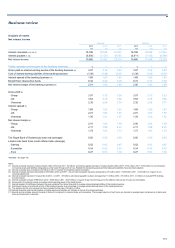

Impairment losses

Impairment losses fell to £5,279 million from £7,437 million in 2011, with

Core impairments falling by £464 million and Non-Core by £1,694 million,

mostly in the Ulster Bank and commercial real estate portfolios.

Impairments represented 1.2% of gross loans and advances excluding

reverse repos compared with 1.5% in 2011.

Risk elements in lending at 31 December 2012 represented 9.1% of

loans and advances excluding reverse repos, compared with 8.6% a year

earlier. Provision coverage was 52%, compared with 49% at 31

December 2011.

Non-operating items

The continuing strengthening RBS’s credit profile resulted in a £4,649

million accounting charge in relation to own credit adjustments versus a

gain of £1,914 million in 2011. This reflected a tightening of more than

340 basis points in the Group’s credit spreads over the year.

The Asset Protection Scheme, which the Group exited from during the

year, was accounted for as a credit derivative and movements in the fair

value of the contract were taken as non-operating items. The APS fair

value charge was £44 million in 2012 bringing the cumulative charge for

the APS to £2.5 billion.

To reflect current experience of Payment Protection Insurance complaints

received, the Group increased its PPI provision by £1,110 million in 2012

compared with £850 million in 2011, bringing the cumulative charge taken

to £2.2 billion, of which £1.3 billion (59%) in redress had been paid by 31

December 2012.

In 2011, the Group recorded an impairment loss of £1,099 million in

respect of its AFS portfolio of Greek government debt. In 2012, the vast

majority of this portfolio was exchanged for Greek sovereign debt and

European Financial Stability Facility notes; the Greek sovereign debt

received in the exchange was sold.

Integration and restructuring costs of £1,415 million increased by £394

million versus £1,021 million in 2011, primarily driven by costs incurred in

relation to the strategic restructuring of Markets and International Banking

(M&IB) that took place during 2012.

Liability management exercises undertaken by the Group during 2012

resulted in a net gain of £454 million (2011 - £255 million).

The UK bank levy is based on the total chargeable equity and liabilities

as reported in the balance sheet at the end of a chargeable period. The

cost of the levy to the Group for 2012 was £175 million compared with

£300 million in 2011.

Interest Rate Hedging Products redress and related costs

Following an industry-wide review conducted in conjunction with the

Financial Services Authority, a charge of £700 million has been booked

for redress in relation to certain interest-rate hedging products sold to

small and medium-sized businesses classified as retail clients under FSA

rules.

Regulatory fines

On 6 February 2013, RBS reached agreement with the Financial

Services Authority, the US Department of Justice and the Commodity

Futures Trading Commission in relation to the setting of LIBOR and other

trading rates, including financial penalties of £381 million. The Group

continues to co-operate with other bodies in this regard and expects it will

incur some additional financial penalties.