RBS 2013 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

133

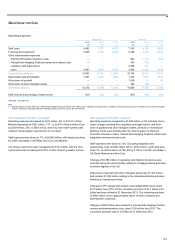

2013 2012 2011

£bn £bn £bn

Capital and balance sheet

Loans and advances to customers (gross)

- mortgages 99.3 99.1 95.0

- personal 8.1 8.8 10.1

- cards 5.8 5.7 5.7

113.2 113.6 110.8

Loan impairment provisions (2.1) (2.6) (2.7)

Net loans and advances to customers 111.1 111.0 108.1

Risk elements in lending 3.6 4.6 4.6

Provision coverage (2) 59% 58% 58%

Customer deposits

- current accounts 32.6 28.9 26.8

- savings 82.3 78.7 75.1

Total customer deposits 114.9 107.6 101.9

A

ssets under management (excluding deposits) 5.8 6.0 5.5

Loan:deposit ratio (excluding repos) 97% 103% 106%

Risk-weighted assets (3)

- credit risk (non-counterparty) 36.1 37.9 41.1

- operational risk 7.8 7.8 7.3

Total risk-weighted assets 43.9 45.7 48.4

Notes:

(1) Divisional return on equity is based on divisional operating profit after tax divided by average notional equity (based on 10% of the monthly average of divisional RWAs, adjusted for capital

deductions).

(2) Provision coverage percentage represents loan impairment provisions as a percentage of risk elements in lending.

(3) Divisional RWAs are based on a long-term conservative average secured mortgage probability of default methodology rather than the current lower point in time basis required for regulatory

reporting.

In March 2013 UK Retail announced its strategy to become a simpler and

more customer-focused business. Investment of £700 million over the

next 3-5 years has been committed to build the best retail bank in the UK.

Good progress has been made with £180 million of investment during

2013 through a number of initiatives directed at enhancing customer

service and simplification of products and services. These have included:

• Improvements to Mobile and Digital Banking which continue to

evolve in line with how customers prefer to conduct their business.

One example of this is the enhancements in the mobile application

allowing customers to pay their mobile phone contacts and obtain

cash without using their debit card with the award winning ‘Get

Cash’. Investment in digital products and services continued in

2013, with 50% of eligible customers now banking online or on

mobile. We currently have 5.6 million online users and 2.9 million

customers using our mobile app with over 100 million transactions

made in 2013. Branch counter transactions were 31 million or 11%

lower across the same period. In addition, UK Retail now has over

2.5 million active mobile users, using the service 28 times a month

on average. Mobile net promoter scores continued to increase in

2013.

• During the year UK Retail invested in the introduction of a new

integrated telephony system, increased training and the professional

development of our staff. We spent more time on each call to

support excellent customer service and to promote relevant

offerings, including self service.

• During Q1 2013 mortgage advisors attended extensive training

courses to help ensure customers receive the best possible

outcome to meet their needs. The training affected balance growth

during H1 2013; however, application volumes have rebounded

quickly with the launch of competitively priced products and the

‘NatYes’ and ‘RBYES’ advertising campaigns leading to H2 2013

applications being 30% higher than H1 2013. RBS was the first bank

to be ready to deliver the second phase of the UK Government’s

Help To Buy scheme, launched in early October 2013. Extended

opening hours in branches helped to deliver more than 3,000

approvals assisting young people and families across Britain buy

their home. Gross mortgage lending increased 3% year-on-year to

£14.3 billion with Q4 2013 25% higher than Q4 2012.