RBS 2013 Annual Report Download - page 259

Download and view the complete annual report

Please find page 259 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

257

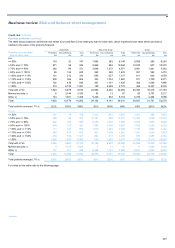

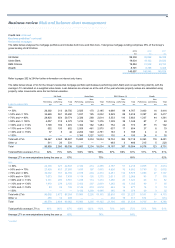

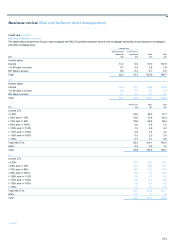

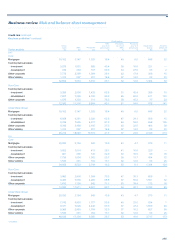

Ulster Bank Rest of the Group Group

Performing Non-performing Total Performing Non-performing Total Performing Non-performing Total

Commercial real estate

loan-to-value ratio £m £m £m £m £m £m £m £m £m

2011

<= 50% 272 32 304 7,091 332 7,423 7,363 364 7,727

> 50% and <= 70% 479 127 606 14,105 984 15,089 14,584 1,111 15,695

> 70% and <= 90% 808 332 1,140 10,042 1,191 11,233 10,850 1,523 12,373

> 90% and <= 100% 438 201 639 2,616 1,679 4,295 3,054 1,880 4,934

> 100% and <= 110% 474 390 864 1,524 1,928 3,452 1,998 2,318 4,316

> 110% and <= 130% 527 1,101 1,628 698 1,039 1,737 1,225 2,140 3,365

> 130% and <= 150% 506 1,066 1,572 239 912 1,151 745 1,978 2,723

> 150% 912 7,472 8,384 433 2,082 2,515 1,345 9,554 10,899

Total with LTVs 4,416 10,721 15,137 36,748 10,147 46,895 41,164 20,868 62,032

Minimal security (1) 72 1,086 1,158 — — — 72 1,086 1,158

Other (2) 193 625 818 8,994 1,844 10,838 9,187 2,469 11,656

Total 4,681 12,432 17,113 45,742 11,991 57,733 50,423 24,423 74,846

Total portfolio average LTV (3) 120% 264% 222% 69% 129% 82% 75% 203% 116%

Notes:

(1) In 2012, the Group reclassified loans with limited (defined as LTV>1,000%) or non-physical security as minimal security, of which a majority were commercial real estate development loans in Ulster

Bank. Total portfolio average LTV is quoted net of loans with minimal security given that the anticipated recovery rate is less than 10%. Provisions are marked against these loans where required to

reflect the relevant asset quality and recovery profile.

(2) Other non-performing loans of £2.3 billion (2012 - £2.0 billion; 2011 - £2.5 billion) were subject to the Group’s standard provisioning policies. Other performing loans of £5.4 billion (2012 - £6.6 billion;

2011 - £9.2 billion) included general corporate loans, typically unsecured, to commercial real estate companies, and major UK house builders in addition to facilities supported by guarantees. The

credit quality of these exposures was consistent with that of the performing portfolio overall.

(3) Weighted average by exposure.

(4) 2012 LTV revised to reflect refinement to security value reporting implemented during 2013.

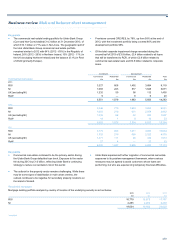

Key points

• The reductions in the higher LTV buckets for the performing book

were offset by the growth in these buckets in the non-performing

book. Ulster Bank Group accounted for the majority of this

deterioration and has addressed this through an increase in

provisions (refer to the section on RCR). Ulster Bank Group's

provision as a percentage of REIL stood at 76% at 31 December

2013 (2012 - 57%). Valuations continued to be affected by difficult,

although improving, market conditions, as well as refinements to the

Group’s estimation approach.

• Interest payable on outstanding loans was covered 3.1x and 1.6x

within UK Corporate and International Banking, respectively, at 31

December 2013 (2012 - 3.0x and 1.5x respectively). The US Retail

& Commercial portfolio is managed on the basis of debt service

coverage, which includes principal amortisation as well as interest

payable. The average debt service coverage was 1.5x at 31

December 2013 (2012 - 1.3x). As a number of different approaches

are used across the Group and across geographies to calculate

interest coverage ratios, they may not be comparable for different

portfolio types and legal entities.

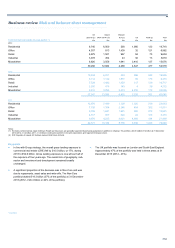

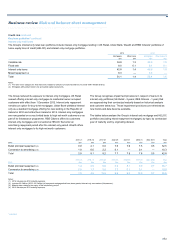

Credit quality metrics relating to commercial real estate lending were as follows:

Group Non-Core

2013 2012 2011 2013 2012 2011

Lending (gross) £52.6bn £63.0bn £74.8bn £19.3bn £26.4bn £34.3bn

Of which REIL £20.1bn £22.1bn £22.9bn £14.3bn £17.1bn £18.8bn

Provisions £13.2bn £10.1bn £9.5bn £10.6bn £8.3bn £8.2bn

REIL as a % of gross loans to customers 38.2% 35.1% 30.6% 74.1% 64.8% 54.8%

Provisions as a % of REIL 66% 46% 41% 74% 49% 44%

Note:

(1) Excludes property related lending to customers in other sectors managed by Real Estate Finance.

Key point

• CRE lending net of impairment provisions decreased by £13.5 billion or 26% in the year to £39.4 billion in part due to the increased impairment

provisions recorded in the fourth quarter of 2013 in Ulster Bank Non-Core, as part of RCR creation and related strategy. Provision coverage on

CRE REIL was 66% compared to 46% at the end of 2012.

Ulster Bank is a significant contributor to Non-Core commercial real estate lending. For further information refer to the section on Ulster Bank Group

(Core and Non-Core).

*unaudited