RBS 2013 Annual Report Download - page 344

Download and view the complete annual report

Please find page 344 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

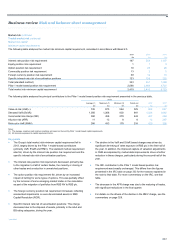

Business review Risk and balance sheet management

342

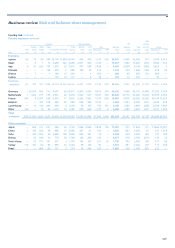

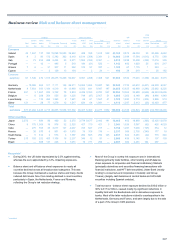

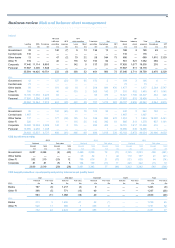

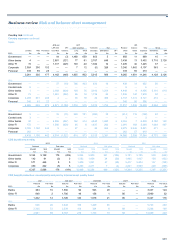

Country risk

Definition

Country risk is the risk of losses occurring as a result of either a country

event or unfavourable country operating conditions. As country events

may simultaneously affect all or many individual exposures to a country,

country event risk is a concentration risk. For other types of concentration

risks such as product, sector or single name concentration, refer to the

Credit risk section.

External environment*

Macroeconomic conditions stabilised in 2013 with signs of improvement

in most mature economies. The US showed the strongest improvement,

with private investment picking up, the housing sector continuing to

strengthen, and unemployment falling. This led the Federal Reserve to

announce in May plans to begin normalising monetary policy. In

December it announced it would start reducing quantitative easing. This

resulted in some volatility in higher-yield asset markets, particularly

emerging markets, where those with the largest external financing needs

saw capital outflows, currency depreciation and stock market losses.

In the second half of the year, investor concerns were heightened by the

risk that the US federal debt ceiling increase would not be passed on time

and that the government might delay debt payments. Short-term political

solutions to these issues were found, though with further progress

needed in 2014.

The eurozone region as a whole remained in recession throughout the

year, but signs of recovery were evident by the second half of the year.

Germany led, but the periphery also showed notable signs of

stabilisation, with Ireland, Spain and Portugal all growing in quarter-on-

quarter terms in the last quarter of 2013. Eurozone monetary policy

support underpinned investor confidence, while progress was made in

developing a banking union that should reduce the risk of a repeat of the

financial crisis over the longer term. Nevertheless, France and Italy

underperformed peers.

In Japan, an economic reform strategy combined with large monetary

stimulus contributed to currency depreciation, a reduction in deflationary

expectations and strong growth in the first half of the year. However,

momentum slowed in the second half of the year.

Many emerging market economies entered 2013 with high growth rates.

While most were in substantially better shape than in previous crises,

some had built up significant imbalances during years of strong capital

inflows. As economic conditions in mature markets, particularly the US,

improved in the course of the year, markets began to anticipate that

monetary policies would normalise.

This led to a sharp round of capital outflows, particularly from equity

markets, in the second quarter of 2013. Currency depreciations in a

number of large emerging economies followed, especially in those with

significant current account deficits. Among the better rated economies,

India, Brazil, Indonesia, South Africa and Turkey, were particularly

affected. To stem the outflow of foreign capital and limit the impact on

domestic asset markets, some countries, including India, started

tightening monetary policy and accelerated financial sector reforms.

Some countries with sizeable accumulated reserve assets, including

China and Russia, were able to use their reserves to ease the pressure

on their currencies.

*unaudited

Outlook

Further strengthening of economic growth in advanced economies is

likely in 2014, but uncertainty over the impact of “tapering” is likely to

contribute to further volatility in asset prices across most regions. The US

is expected to perform quite strongly, with the eurozone also likely to

continue its uneven recovery, although in both cases key areas of the

economy will remain fragile. A more challenging year for emerging

economies is expected as net capital inflows decline, resulting in more

pronounced market volatility and differentiation. Further policy tightening

is likely and growth rates are set to slow, especially in the weakest

markets.

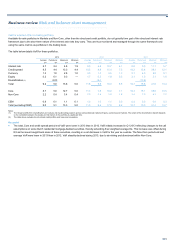

Sources of risk

Country risk has the potential to affect all parts of the Group’s portfolio

across wholesale and retail activities that are directly or indirectly linked

to the country in question.

It arises from possible economic or political events in each country to

which the Group has exposure, and from unfavourable conditions

affecting daily operations in a country.

Country events may include a sovereign default, political conflict, banking

crisis or deep and prolonged recession leading to possible counterparty

defaults. Transfer or convertibility restrictions imposed by a country’s

government to stem the loss of foreign currency reserves may

temporarily prevent counterparties from meeting their payment

obligations. Major currency depreciation may also affect a customer’s

income or debt burden, leading to default.

Unfavourable operating conditions may include the risk that a weak or

creditor unfriendly legal system within a country makes it difficult for the

Group to recover its claims in the event of customer default. An unreliable

or unstable political system may lead to sudden compliance or

reputational issues for the Group, or even expropriation without proper

compensation.

Governance*

The Group’s country risk framework is set by the Executive Risk Forum

(ERF). This body delegates authority to the Group Country Risk

Committee (GCRC) to decide on country risk matters, including risk

appetite, risk management strategy and framework, risk exposure and

policy, as well as sovereign ratings, sovereign loss given default rates

and country Watchlist colours. The GCRC, which is chaired by the Head

of Global Country Risk (GCoR) and includes representatives of divisions

with country risk exposures, can escalate issues when necessary to the

ERF.

For further information on governance, refer to the Risk governance

section on page 175.