RBS 2013 Annual Report Download - page 528

Download and view the complete annual report

Please find page 528 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

518 -

519

519 -

520

520 -

521

521 -

522

522 -

523

523 -

524

524 -

525

525 -

526

526 -

527

527 -

528

528 -

529

529 -

530

530 -

531

531 -

532

532 -

533

533 -

534

534 -

535

535 -

536

536 -

537

537 -

538

538 -

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

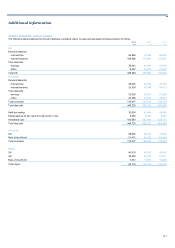

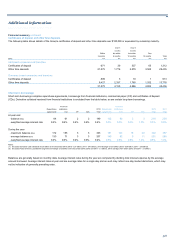

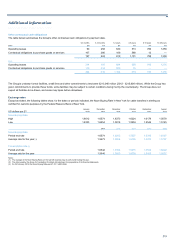

Additional information

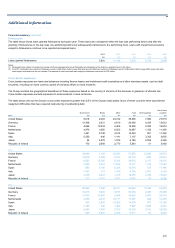

526

Risk factors continued

The Group has significant exposure to a weakening of the nascent

economic recovery in Europe

In Europe, countries such as Ireland, Italy, Greece, Portugal and Spain

have been particularly affected by the recent macroeconomic and

financial conditions. Although the risk of sovereign default continued to

decline in 2013 due to the continuing actions of the European Central

Bank (ECB) and the EU, the risk of default remains and yields on the

sovereign debt of many EU member states have remained well above

pre-crisis levels. This default risk raises concerns, and the possibility

remains that the contagion effect spreads to other EU economies,

including the UK economy, that the euro could be abandoned as a

currency by one or more countries that have already adopted its use, or

in an extreme scenario, that the abandonment of the euro could result in

the dissolution of the European Monetary Union (EMU). This would lead

to the re-introduction of individual currencies in one or more EMU

member states.

The effects on the UK, European and global economies of any potential

dissolution of the EMU, exit of one or more EU member states from the

EMU and the redenomination of financial instruments from the euro to a

different currency, are impossible to predict fully. However, if any such

events were to occur they would likely:

• result in significant market dislocation;

• heighten counterparty risk;

• result in downgrades of credit ratings for European borrowers, giving

rise to increases in credit spreads and decreases in security values;

• disrupt and adversely affect the economic activity of the UK and

other European markets; and

• adversely affect the management of market risk and in particular

asset and liability management due, in part, to redenomination of

financial assets and liabilities and the potential for mismatch.

The occurrence of any of these events would have a material adverse

effect on the Group’s financial condition, results of operations and

prospects.

The Group has significant exposure to private sector and public sector

customers and counterparties in the eurozone (at 31 December 2013

principally Ireland (£39.8 billion), Germany (£31.1 billion), The

Netherlands (£25.9 billion), France (£23.8 billion), Spain (£11.2 billion)

and Italy (£7.1 billion)). The Group’s private and public sector exposures

in the eurozone have been, and may in the future be, affected by credit

losses and restructuring of their terms, principal, interest and maturity. In

2011, this included an impairment loss of £1.1 billion in respect of its

holding of Greek government bonds. The public sector exposure

comprises exposure to central and local governments and deposits with

central banks. At 31 December 2013, the Group’s eurozone government

debt exposure amounted to £15.9 billion (largely AFS and HFT debt

securities exposure) including aggregate exposure of £2.8 billion to

Ireland, Spain, Italy, Portugal Greece and Cyprus (largely net HFT debt

securities exposure to Italy and Spain).

The Group and its UK bank subsidiaries are subject to the provisions of

the Banking Act 2009, as amended by the Banking Reform Act 2013,

which includes special resolution powers including nationalisation and

bail-in

Under the Banking Act 2009, substantial powers have been granted to

HM Treasury, the Bank of England and the Prudential Regulation

Authority (PRA) and Financial Conduct Authority (FCA) (together, the

“Authorities”) as part of a special resolution regime. These powers enable

the Authorities to deal with and stabilise certain deposit-taking UK

incorporated institutions that are failing, or are likely to fail, to satisfy the

threshold conditions (within the meaning of section 41 of the Financial

Services and Markets Act 2000 (FSMA), which are the conditions that a

relevant entity must satisfy in order to obtain its authorisation to perform

regulated activities). The special resolution regime consists of three

stabilisation options: (i) transfer of all or part of the business of the

relevant entity and/or the securities of the relevant entity to a private

sector purchaser, (ii) transfer of all or part of the business of the relevant

entity to a ‘bridge bank’ wholly owned by the Bank of England and (iii)

temporary public ownership (nationalisation) of the relevant entity. If HM

Treasury decides to take the Group into temporary public ownership

pursuant to the powers granted under the Banking Act 2009, it may take

various actions in relation to any securities without the consent of holders

of the securities.

Among the changes introduced by the Banking Reform Act 2013, the

Banking Act 2009 is amended to insert a bail-in option as part of the

powers of the UK resolution authority which option will come into force on

such date as shall be stipulated by HM Treasury. The bail-in option will

be introduced as an additional power available to the Bank of England to

enable it to recapitalise a failed institution by allocating losses to its

shareholders and unsecured creditors in a manner that seeks to respect

the hierarchy of claims in liquidation. The bail-in option includes the

power to cancel a liability, to modify the form of a liability (including the

power to convert a liability from one form to another) or to provide that a

contract under which the institution has a liability is to have effect as if a

specified right had been exercised under it, each for the purposes of

reducing, deferring or cancelling the liabilities of the bank under

resolution, as well as to transfer a liability. The Banking Reform Act 2013

is consistent with the range of tools that Member States will be required

to make available to their resolution authorities under the Recovery and

Resolution Directive (RRD), although since the RRD remains in draft

form, there can be no assurance that the bail-in option added under the

Banking Reform Act will not need to change to comply with the RRD.

The Group is subject to a variety of risks as a result of implementing the

State Aid restructuring plan

The Group was required to obtain State Aid approval for the aid given to

the Group by HM Treasury as part of the placing and open offer

undertaken by the Group in December 2008, the issuance to HM

Treasury of £25.5 billion of B shares in the capital of the Group which are,

subject to certain terms and conditions, convertible into ordinary shares in

the share capital of the Group and a contingent commitment by HM

Treasury (which has now been terminated) to subscribe for up to an

additional £8 billion of B Shares if certain conditions are met in addition to

the Group’s participation in the Asset Protection Scheme (APS) (which

has now been terminated). In that context, as part of the terms of the

State Aid approval, the Group, together with HM Treasury, agreed the

terms of a restructuring plan.