RBS 2013 Annual Report Download - page 244

Download and view the complete annual report

Please find page 244 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

242

Credit risk continued

Early problem identification and problem debt management

Wholesale

Early problem identification

Each division has defined early warning indicators (EWIs) to identify

customers experiencing financial difficulty, and to increase monitoring if

needed. EWIs may be internal, such as a customer’s bank account

activity, or external, such as a publicly-listed customer’s share price. If

EWIs show a customer is experiencing potential or actual difficulty,

divisional credit officers may decide to place it on the Watchlist.

Watchlist*

There are three Watch classifications - Amber, Red and Black - reflecting

progressively deteriorating conditions. Watch Amber customers are

performing customers who show early signs of potential financial

difficulty, or have other characteristics that warrant closer monitoring.

Watch Red customers are performing customers who show signs of

declining creditworthiness which requires active management usually by

the Global Restructuring Group (GRG). Watch Black customers include

risk elements in lending and potential problem loans.

Once on the Watchlist, customers are subject to heightened scrutiny.

Depending on the severity of the financial difficulty and the size of the

exposure, the customer relationship strategy is reassessed by credit

officers, by specialist units in divisions or by GRG. In more material

cases, a forum of experienced credit, portfolio management and remedial

management specialists in the divisions or GRG may reassess the

customer relationship strategy. In accordance with Group-wide policies, a

number of mandatory actions are taken, including a review of the

customer’s credit grade and facility and security documentation.

Other appropriate corrective action is taken when circumstances emerge

that may affect the customer’s ability to service its debt. Such

circumstances include deteriorating trading performance, imminent

breach of covenant, challenging macroeconomic conditions, a late

payment or the expectation of a missed payment.

For all Watch Red cases, the division is required to consult with GRG on

whether the relationship should be transferred to GRG (for more

information on GRG, refer to below). Watch Red customers that continue

to be managed by the divisions tend to be those requiring subject matter

expertise that is available in the divisions rather than in GRG.

At 31 December 2013, exposures to customers reported as Watchlist

Red and managed in the divisions totalled £3.2 billion (2012 - £4.3

billion).

Remediation strategies available in the divisions include granting a

customer various types of concessions. Any decision to approve a

concession will be a function of the division’s specific country and sector

appetite, the key metrics of the customer, the market environment and

the loan structure and security. For further information, refer to the

Wholesale forbearance section below.

Other potential outcomes of the relationship review are to: take the

customer off the Watchlist; offer additional lending and continue

monitoring; transfer the relationship to GRG if appropriate; or exit the

relationship altogether.

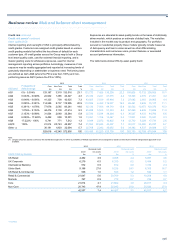

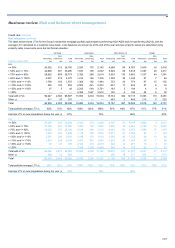

The following table shows a sector breakdown of CRA of Watch Red customers under GRG management:

2013 2012 2011

Core Non-Core Total Core Non-Core Total Core Non-Core Total

Watch Red CRA by current exposure £m £m £m £m £m £m £m £m £m

Property 3,178 1,841 5,019 5,605 4,377 9,982 6,561 6,011 12,572

Transport 1,791 456 2,247 2,238 478 2,716 1,159 2,252 3,411

Retail and leisure 1,092 237 1,329 1,542 432 1,974 1,528 669 2,197

Services 955 40 995 870 84 954 808 141 949

Other 2,312 804 3,116 3,087 1,177 4,264 1,952 916 2,868

Total 9,328 3,378 12,706 13,342 6,548 19,890 12,008 9,989 21,997

The decrease in Watch Red cases was driven predominantly by a lower

flow of cases into GRG, repayments and movement of cases into Watch

Black. The overall value of customers in default has however reduced

during the year. For further information regarding the asset quality of the

Group's portfolio refer to the Asset quality section on page 236.

Global Restructuring Group

GRG manages the Group’s wholesale problem debt portfolio in cases

where its exposure to the customer exceeds £1 million. In addition, GRG

provides a specialist credit function, the Strategy Management Unit, for

distressed bilateral lending where the exposure is between £250,000 and

£1 million. The primary function of GRG is to restore customers to an

acceptable credit condition and minimise losses to the Group.

*unaudited

The factor common to all customers managed by GRG is that the

Group’s exposure is outside risk appetite. Customers transferred to GRG

typically show symptoms of significant financial difficulty, such as cash

flow pressures, or show evidence that the management team has limited

experience of managing a business in difficulty. In addition, a customer

may be transferred to GRG if the Group is not provided with sufficient or

reliable information on which to make decisions.

GRG relationship managers use their skill, experience and judgement to

support customers through these difficulties while seeking to minimise

losses to protect the Group’s capital.