RBS 2013 Annual Report Download - page 236

Download and view the complete annual report

Please find page 236 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

234

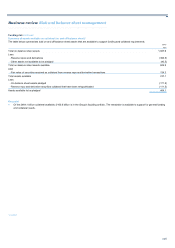

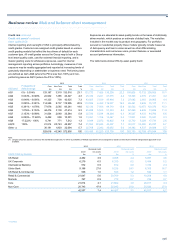

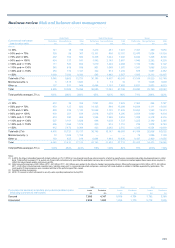

Credit risk continued

Credit risk assets* continued

Key points

Financial markets and the Group’s focus on risk appetite and sector

concentration had a direct impact on the portfolio during the year with the

following key trends observed:

• Total CRA fell 8%, with the only notable increase being in the

sovereign sector, including exposures to central banks (increased

3%). Excluding sovereign exposures, CRA decreased by 10%.

• At the year end, the portfolio comprised 31% personal exposure

(2012 - 29%), sovereign 15% (2012 - 13%) exposure to banks and

other financial institutions 16% (2012 - 18%), property 13% (2012 -

14%), and other corporate sectors 25% (2012 - 26%).

• CRA fell in all geographic regions. The largest decrease, in Western

Europe, was primarily a result of reduced exposures to European

central banks.

• UK exposure increased to 56% of CRA (2012 - 51%) because of a

£16.2 billion rise in exposure to the Bank of England. This was offset

predominantly by falls in Non-Core property (£7.5 billion) and Core

personal and banking sectors, which fell £4.3 billion in total.

Excluding sovereigns, UK Core exposure fell by 3%).

• The personal sector, excluding exposures in North America, fell by

2% due to reduced overdraft and lending exposure in the UK. This

was offset by slightly increased UK mortgage exposure. Personal

exposure in North America decreased disproportionately due to

Non-Core exposures.

• Exposure to sovereigns fluctuates according to Group liquidity

requirements and cash positions. These are driven by inflows and

outflows of deposits which determine the level of cash placed with

central banks and have contributed to higher exposures at the Bank

of England and lower exposures at European central banks. The

Group’s sovereign portfolio comprises exposures to central

governments, central banks and sub-sovereigns such as local

authorities, primarily in the Group’s key markets of the UK, Western

Europe and the US. The asset quality is high because exposures

are largely short-term cash balances placed with central banks such

as the Bank of England, the Federal Reserve and the Eurosystem

(including the European Central Bank and central banks in the

eurozone). Information on the Group’s exposure to governments,

including peripheral eurozone sovereigns, can be found in the

Country risk section.

• Exposure to the banking sector is well diversified geographically.

Limits and exposures are tightly controlled through the combination

of the SNC framework, bespoke credit policies and country limits.

Derivatives generated the largest exposure for banks (58% of credit

risk assets in the banks sector), but a large portion of the exposures

was collateralised. The increase in bank exposure in the Asia Pacific

region was largely driven by short-term, trade finance related

activities.

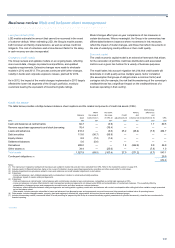

*unaudited

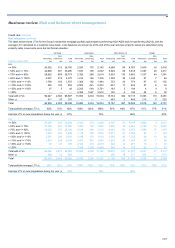

• Exposure to banks and financial institutions declined by 20%. This

was primarily as a result of limited lending and interbank money

market activity which fell by 8% and a reduction in derivative

exposures which fell by 27%. The declining trend in interbank

activity was largely attributable to increased bank liquidity including

access to liquidity via schemes put in place via central banks and

governments. The reduction in derivative exposure was due to the

Group exiting certain products and the benefits of regulatory netting

derived from the implementation of new modelling methodology. The

Group has a suite of control frameworks and policies for managing

the derivatives portfolio, particularly uncollateralised derivatives with

long tenors. During the year the control framework for this segment

of the portfolio was further tightened.

• Exposure to other financial institutions comprises a range of

financial companies, the largest of which were funds (25%)

securitisation vehicles (22%) and financial intermediaries (16%)

including broker dealers and central counterparties (CCPs). The

Core other financial institutions portfolio decreased by 8% in 2013.

The Non-Core portfolio decreased by 31%.

• At the year end, the total exposure to CCPs was £4.1 billion (2012 -

£3.2 billion). Regulatory initiatives to encourage the wider use of

CCPs for clearing over-the-counter derivatives across the industry

continue. The Group supports this move but recognises that its

concentration risk to CCPs will continue to rise when it clears its own

trades, as well as when it acts as a clearing broker for third

parties. This increased concentration risk is being managed under a

specific risk appetite and control framework. The Group’s CCP

exposure remains dominated by a small number of well-established,

high quality and reputable clearing houses.

• The Group continued to manage down its exposures to financial

guarantors - credit derivative products companies (CDPCs) and

monolines with a view to exiting these portfolios. Exposure to

financial guarantors declined by 69% and represented less than 1%

of the other financial institutions portfolio (2012 - 2%). Exposures

have decreased materially over time as trades are commuted and

exposures reduced due to the tightening credit spread of the assets

protected by CDPCs and monolines. At the year end, exposures to

CDPCs and monolines totalled £274 million (2012 - £874 million).

• The majority of the Group’s property exposure was commercial real

estate in Ireland and the UK (refer to Commercial real estate on

pages 252 to 257 for further details). The remainder comprised

lending to construction companies and building materials groups,

which fell by £1.7 billion (15%), and housing associations, which

increased by £0.9 billion (12%). A total of 59% of the Group’s Core

property exposure was in UK Corporate (2012 - 60%) with Ulster

Bank and US Retail & Commercial representing 10% and 9%

respectively, unchanged from 2012.