RBS 2013 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

193

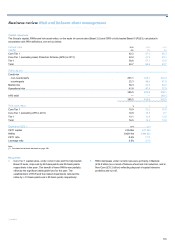

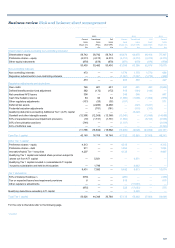

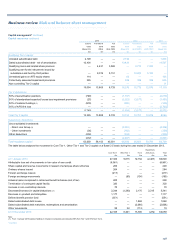

Capital management*

Definition

The Group aims to maintain an appropriate level of capital to meet its

business needs and regulatory requirements, and operates within an

agreed risk appetite. The appropriate level of capital is determined based

on the dual aims of: (i) meeting minimum regulatory capital requirements;

and (ii) ensuring the Group maintains sufficient capital to uphold

customer, investor and rating agency confidence in the organisation,

thereby supporting the business franchise and funding capacity.

2013 overview

The Group reported a Core Tier 1 ratio of 10.9% as at 31 December

2013. On a fully loaded Basel III basis, the Group’s equivalent Common

Equity Tier 1 (CET1) ratio was 8.6%.

The Group’s Core Tier 1 ratio is higher than at the end of 2012 despite

absorbing changes to credit model parameters and in the face of

challenging economic headwinds and continuing costs of de-risking. This

has been achieved through a continued focus on reshaping the Group’s

use of capital with the Group announcing in November 2013

management actions to accelerate the building of its capital strength. The

measures include creation of an internal 'bad bank' to accelerate the run-

down of high risk assets of £29 billion funded assets at the end of 2013.

Faster run-down of high risk assets entails accelerated and increased

impairments and other adjustments in the fourth quarter of 2013, but the

capital impact of this is significantly reduced by a commensurate

reduction in expected loss capital deductions. The management strategy

will result in a strengthening of the Group's capital ratios in the medium

term.

The Group continues to target a fully loaded Basel III CET1 ratio of c.11%

by the end of 2015 and 12% or above by the end of 2016.

The Group has announced plans to accelerate the divestment of RBS

Citizens. Preparations for a partial initial public offering in 2014 are on

track and the Group intends to fully divest the business by the end of

2016, benefiting CET1.

The Group continues to meet the minimum leverage ratio under both the

Basel III and Capital Requirements Regulation (CRR) bases.

Focus for the Group remains on active de-risking of the balance sheet to

meet strategic objectives, demonstrated in the leverage exposure

measure by Non-Core asset disposal and run-off, and the downsizing of

Markets business.

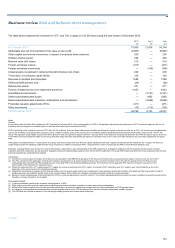

Regulatory developments

CRD IV

The European Union has implemented the Basel III proposals through

the CRR and the Capital Requirements Directive (CRD), collectively

known as CRD IV. CRD IV was implemented on 1 January 2014. The

European Banking Authority’s technical standards which will provide

clarification of the CRD IV, are still to be finalised through adoption by the

European Commission and implemented within the UK.

*unaudited

The Prudential Regulatory Authority (PRA) announced the acceleration of

the end state rules for CET1 capital, whereby from 1 January 2014 the

calculation is now closely aligned with the fully loaded definition. There

will be no transitional arrangements applied to the prudential filters or

regulatory deductions with the exception of unrealised gains on available

for sale debt and equity which will be incorporated from 1 January 2015.

CRD IV and Basel III will impose a minimum CET1 ratio of 4.5% of

RWAs. There are three buffers which will affect the Group: the capital

conservation buffer set at 2.5%; the counter-cyclical capital buffer (up to

2.5% of RWAs), to be applied when macroeconomic conditions indicate

areas of the economy are over-heating; and the Global-Systemically

Important Bank buffer currently set at 1.5% for the Group. The regulatory

target capital requirements will be phased in and are expected to apply in

full from 1 January 2019, in the meantime using national discretion the

PRA can apply a top-up. As set out in the PRA’s Supervisory Statement

SS3/13, the Group and other major UK banks and building societies are

required to meet a CET1 ratio of 7% after taking into account certain

adjustments set by the PRA.

PRA guidance indicates that from 1 January 2015, the Group must meet

at least 56% of its Pillar 2A capital requirement with CET1 capital and the

balance with Additional Tier 1 capital. The Pillar 2A capital requirement is

the additional capital that the Group must hold, in addition to meeting its

Pillar 1 requirements in order to comply with the PRA’s overall financial

adequacy rule.

Subordinated debt instruments which do not meet the new eligibility

criteria will be grandfathered on a reducing basis over ten years.

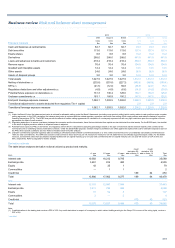

Governance

Governance and approach

The Group Asset and Liability Management Committee (GALCO) is

responsible for ensuring the Group maintains adequate capital at all

times. The Capital and Stress Testing Committee (CAST) is a cross-

functional body driving and directing integrated risk capital activities

including determination of the amount of capital the Group should hold,

how and where capital is allocated and planning for actions that would

ensure that an adequate capital position would be maintained in a

stressed environment. These activities have linkages to capital planning,

risk appetite and regulatory change. CAST reports through GALCO and

comprises senior representatives from Risk Management, Group Finance

and Group Treasury. Target capital ratios are set and monitored by the

PRA for the Group. Management of capital is achieved by supervision of

forecast capital and RWA over a five year time horizon.

Pillar 3

The Group’s Pillar 3 disclosures provide additional analysis of exposure

at default and credit risk measures such as credit risk mitigation,

counterparty credit risk and provisions and their associated RWAs under

the various Basel II approaches.