RBS 2013 Annual Report Download - page 415

Download and view the complete annual report

Please find page 415 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

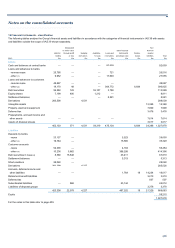

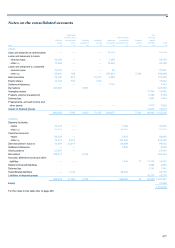

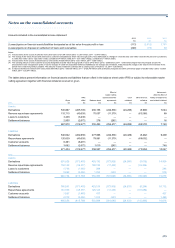

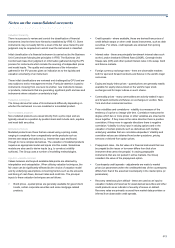

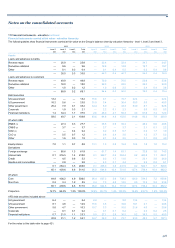

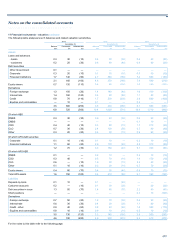

Notes on the consolidated accounts

413

Valuation hierarchy

There is a process to review and control the classification of financial

instruments into the three level hierarchy established by IFRS 13. Some

instruments may not easily fall into a level of the fair value hierarchy and

judgment may be required as to which level the instrument is classified.

Initial classification of a financial instrument is carried out by the Business

Unit Control team following the principles in IFRS. The Business Unit

Control team base their judgment on information gathered during the IPV

process for instruments which include the sourcing of independent prices

and model inputs. The quality and completeness of the information

gathered in the IPV process gives an indication as to the liquidity and

valuation uncertainty of an instrument.

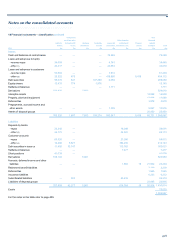

These initial classifications are reviewed and challenged by GPU and are

also subject to senior management review. Particular attention is paid to

instruments crossing from one level to another, new instrument classes

or products, instruments that are generating significant profit and loss and

instruments where valuation uncertainty is high.

Valuation techniques

The Group derives fair value of its instruments differently depending on

whether the instrument is a non-modelled or a modelled product.

Non-modelled products

Non-modelled products are valued directly from a price input and are

typically valued on a position by position basis and include cash, equities

and most debt securities.

Modelled products

Modelled products are those that are valued using a pricing model,

ranging in complexity from comparatively vanilla products such as

interest rate swaps and options (e.g. interest rate caps and floors)

through to more complex derivatives. The valuation of modelled products

requires an appropriate model and inputs into this model. Sometimes

models are also used to derive inputs (e.g. to construct volatility

surfaces). The Group uses a number of modelling methodologies.

Inputs to valuation models

Values between and beyond available data points are obtained by

interpolation and extrapolation. When utilising valuation techniques, the

fair value can be significantly affected by the choice of valuation model

and by underlying assumptions concerning factors such as the amounts

and timing of cash flows, discount rates and credit risk. The principal

inputs to these valuation techniques are as follows:

• Bond prices - quoted prices are generally available for government

bonds, certain corporate securities and some mortgage-related

products.

• Credit spreads - where available, these are derived from prices of

credit default swaps or other credit based instruments, such as debt

securities. For others, credit spreads are obtained from pricing

services.

• Interest rates - these are principally benchmark interest rates such

as the London Interbank Offered Rate (LIBOR), Overnight Index

Swaps rate (OIS) and other quoted interest rates in the swap, bond

and futures markets.

• Foreign currency exchange rates - there are observable markets

both for spot and forward contracts and futures in the world's major

currencies.

• Equity and equity index prices - quoted prices are generally readily

available for equity shares listed on the world's major stock

exchanges and for major indices on such shares.

• Commodity prices - many commodities are actively traded in spot

and forward contracts and futures on exchanges in London, New

York and other commercial centres.

• Price volatilities and correlations - volatility is a measure of the

tendency of a price to change with time. Correlation measures the

degree which two or more prices or other variables are observed to

move together. If they move in the same direction there is positive

correlation; if they move in opposite directions there is negative

correlation. Volatility is a key input in valuing options and in the

valuation of certain products such as derivatives with multiple

underlying variables that are correlation-dependent. Volatility and

correlation values are obtained from broker quotations, pricing

services or derived from option prices.

• Prepayment rates - the fair value of a financial instrument that can

be prepaid by the issuer or borrower differs from that of an

instrument that cannot be prepaid. In valuing prepayable

instruments that are not quoted in active markets, the Group

considers the value of the prepayment option.

• Counterparty credit spreads - adjustments are made to market

prices (or parameters) when the creditworthiness of the counterparty

differs from that of the assumed counterparty in the market price (or

parameters).

• Recovery rates/loss given default - these are used as an input to

valuation models and reserves for asset-backed securities and other

credit products as an indicator of severity of losses on default.

Recovery rates are primarily sourced from market data providers or

inferred from observable credit spreads.