RBS 2013 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

152

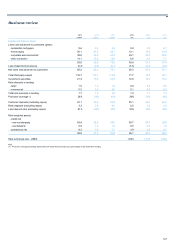

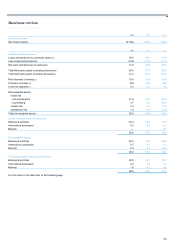

Markets continued

In 2013, Markets launched and executed a strategic repositioning of the

business, aimed at reducing risk, tightening controls, consolidating the

geographic footprint and reducing complexity by refocusing on the

franchise’s core strengths in fixed income products. The division met or

exceeded all internal targets for reducing controllable costs, risk weighted

assets and balance sheet, while meeting revenue and operating profit

expectations. Controls were enhanced, trading was integrated into four

financial hubs, the front-to-back operating model was simplified and an

agreement was reached for the sale of the Investor Products and Equity

Derivatives business. Market share in the four core product areas (Rates,

Currencies, Asset Backed Products and Credit) remained broadly stable

with high profile client transactions executed across the globe. As a result

of the strategic repositioning, Markets ended 2013 better positioned for

the changing regulatory and external environment.

Lower income in 2013 compared with 2012 reflected both the strategic

scaling back of the balance sheet and risk reduction in a difficult market

environment. Client activity was limited by the uncertainty that

surrounded the much anticipated tapering of the Federal Reserve’s

programme of quantitative easing. This contrasted with 2012 when

markets were boosted by the European Central Bank’s Long Term

Refinancing Operation. Nevertheless, Markets’ core businesses

remained resilient and continued to produce positive results. Currencies

income increased significantly year on year and Corporate Debt Capital

Markets reaffirmed its leading position in the GBP market.

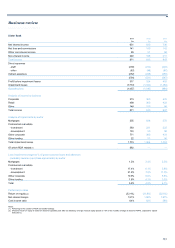

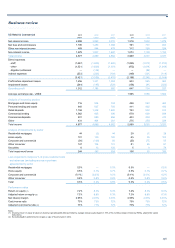

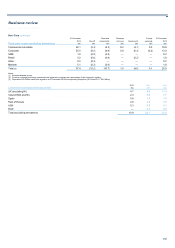

2013 compared with 2012

Operating profit fell by £889 million with income falling by 26%, partly

offset by significant cost reductions. The de-risking of Markets resulted in

a 36% reduction in risk-weighted assets.

Rates actively repositioned the business during 2013, lowering the

balance sheet and reducing risk. This, combined with a weak trading

performance in H1 2013, resulted in subdued returns.

Currencies income increased as the franchise remained resilient and FX

Options benefited from opportunities in volatile FX and emerging

markets.

Asset Backed Products continued to perform well, although income was

affected by investor concerns regarding tapering of the Federal Reserve’s

programme of quantitative easing and a reduction in the balance sheet

and risk resources deployed by the business.

Credit Markets reflected the previous year’s de-risking of credit trading

and witnessed a modest reduction in Debt Capital Markets income,

although the business executed a number of significant transactions and

retained its leading position in corporate GBP issuance.

Costs fell by 11%, reflecting a reduction in headcount of 1,000 – split

evenly between the front and back-office - and tightly controlled

discretionary expenses, although this was offset by a higher level of legal

costs, primarily related to legacy issues in the US Asset Backed Products

business.

The increase in impairments was driven predominantly by provisions

against a single exposure in 2013.

Reducing risk and refocusing the division on core fixed income and

currencies products drove a substantial reduction in both balance sheet

and risk capital. Third party assets were £72 billion lower than 31

December 2012 and risk-weighted assets, at £65 billion, were down £37

billion.

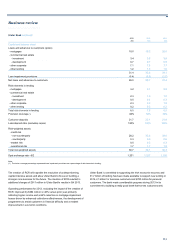

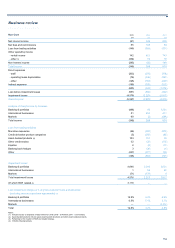

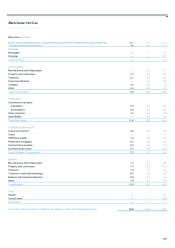

2012 compared with 2011

Operating profit increased by 68% reflecting 2% growth in income and

20% decrease in direct expenses, most notably through a reduction in

staff costs.

Rates benefited from a strong trading performance, while losses incurred

in managing counterparty exposures during the third quarter of 2011

were not repeated during 2012. Revenues for the year were up 32% to

£1.9 billion.

Currencies volumes were weak across the industry, although the Spot FX

business minimised the impact on revenue. Options income was limited

by further Eurozone uncertainty.

Asset Backed Products continued to perform strongly as markets were

sustained throughout the year by investors’ search for yield. Revenues

for the year were £1.3 billion, up 8% from a strong performance of £1.22

billion in 2011.

A 59% increase in Credit Markets revenue to £735 million was driven by

Flow Credit which, as a result of improved risk management and more

benign market conditions, recorded good profitability compared with a

loss in 2011. This was partially offset by weaker earnings from credit

origination.

The division focused on controlling costs throughout 2012, driving total

expenses down by 16%. Lower staff expenses, down 26%, reflect lower

headcount and lower levels of variable compensation, including

reductions and clawbacks following the Group’s LIBOR settlements

reached on 6 February 2013, with the compensation ratio falling from

44% to 32%. Headcount reductions totalled 2,700 in the year, including

that resulting from the exit of businesses announced in January. Other

expenses fell by 3% as rigorous controls on discretionary expenditure

and the exiting of product areas continued to take effect, partially offset

by higher legal expenses.

The reduction in third party assets reflected management action to

optimise and de-risk the balance sheet, consistent with previously

disclosed medium-term objectives.

The division reduced risk-weighted assets, successfully focusing on

lowering risk and enhancing models whilst managing the requirement for

greater prudence in the regulatory environment.

Not reflected in Markets operating results in 2012 were the following

items: £381 million for regulatory fines; £350 million for its share of the

provision for interest rate swap redress; and approximately £700 million

in restructuring costs associated with the strategic changes that took

place during 2012.