RBS 2013 Annual Report Download - page 429

Download and view the complete annual report

Please find page 429 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

435 -

436

436 -

437

437 -

438

438 -

439

439 -

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Notes on the consolidated accounts

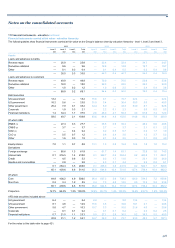

427

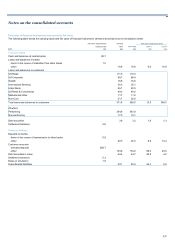

Other unique trades are valued using a specialised model for each

instrument and the same market data inputs as all other trades where

applicable. By their nature, the valuation is also driven by a variety of

other model inputs, many of which are unobservable in the market.

Where these instruments have embedded optionality they are valued

using a variation of the Black-Scholes option pricing formula, and where

they have correlation exposure they are valued using a variant of the

Gaussian Copula model. The volatility or unique correlation inputs

required to value these products are generally unobservable and the

instruments are therefore deemed to be level 3 instruments.

Equity derivatives

Equity derivative products are analysed into equity exotic derivatives and

equity hybrids. Exotic equity derivatives have payouts based on the

performance of one or more stocks, equity funds or indices. Most payouts

are based on the performance of a single asset and are valued using

observable market option data. Unobservable equity derivative trades are

typically complex basket options on stocks. Such basket option payouts

depend on the performance of more than one equity asset and require

correlations for their valuation. Valuation is then performed using industry

standard valuation models, with unobservable correlation inputs

calculated by reference to correlations observed between similar

underlyings.

Equity hybrids have payouts based on the performance of a basket of

underlyings where underlyings are from different asset classes.

Correlations between these different underlyings are typically

unobservable with no market information on closely related assets

available. Where no market for the correlation input exists, these inputs

are based on historical time series.

Interest rate and commodity derivatives

Interest rate and commodity options provide a payout (or series of

payouts) linked to the performance of one or more underlying, including

interest rates, foreign exchange rates and commodities.

Exotic options do not trade in active markets except in a small number of

cases. Consequently, the Group uses models to determine fair value

using valuation techniques typical for the industry. These techniques can

be divided firstly into modelling approaches and secondly, into methods

of assessing appropriate levels for model inputs. The Group uses a

variety of proprietary models for valuing exotic trades.

Exotic valuation inputs include the correlation between interest rates,

foreign exchange rates and commodity prices. Correlations for more

liquid rate pairs are valued using independently sourced consensus

pricing levels. Where a consensus pricing benchmark is unavailable,

these instruments are classified as level 3.

The carrying value of debt securities in issue is represented partly by

underlying cash and partly through a derivative component. The

classification of the amount in level 3 is driven by the derivative

component and not by the cash element.

Other financial instruments

In addition to the portfolios discussed above, there are other financial

instruments which are held at fair value determined from data which are

not market observable, or incorporating material adjustments to market

observed data.

Other considerations

Valuation adjustments

CVA applied to derivative exposures to other counterparties and own

credit adjustments applied to derivative liabilities (DVA) are calculated on

a portfolio basis. Whilst the methodology used to calculate each of these

adjustments references certain inputs which are not based on observable

market data, these inputs are not considered to have a significant effect

on the net valuation of the related portfolios. The classification of the

derivative portfolios which the valuation adjustments are applied to is not

determined by the observability of the valuation adjustments, and any

related sensitivity does not form part of the level 3 sensitivities presented.

Funding related adjustments

The discount rates applied to derivative cash-flows in determining fair

value reflect any underlying collateral agreements. Collateralised

derivative exposures are generally discounted at the relevant OIS rates

whilst funding valuation adjustments are applied to uncollateralised

derivative exposures. Whilst these adjustments reference certain inputs

which are not based on observable market data, these inputs are not

considered to have a significant effect on the valuation of the individual

trades. The classification of derivatives is not determined by the

observability of these adjustments, and any related sensitivity does not

form part of the level 3 sensitivities presented.

Own credit - issued debt

For structured notes issued the own credit adjustment is based on debt

issuance spreads above average inter-bank rates at the reporting date (at

a range of tenors). Whilst certain debt issuance spreads are not based on

observable market data, these inputs are not considered to have a

significant effect on the valuation of individual trades. Neither the

classification of structured notes issued nor any related valuation

sensitivities are determined by the observability of the debt issuance

spreads.