RBS 2013 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

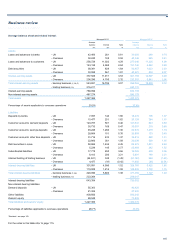

Business review

106

Competition

The Group faces strong competition in all the markets it serves. Banks’

balance sheets have strengthened whilst loan demand remains subdued

as many customers continue to deleverage even as the UK economy

begins to show signs of recovery. Competition for retail deposits has

eased somewhat as institutions have made progress towards building

strong and diverse funding platforms for their balance sheets.

Competition for corporate and institutional customers in the UK and

abroad is from UK banks and from large foreign universal banks that offer

combined investment and commercial banking capabilities. In addition,

the Group’s Markets division faces strong competition from dedicated

investment banks. In asset finance, the Group competes with banks and

specialist asset finance providers, both captive and non-captive. In

European and Asian corporate and institutional banking markets the

Group competes with the large domestic banks active in these markets

and with the major international banks.

In the small business banking market, the Group competes with other UK

clearing banks, specialist finance providers and building societies.

In the personal banking segment, the Group competes with UK clearing

banks and building societies, major retailers and life assurance

companies. In the mortgage market, the Group competes with UK

clearing banks and building societies. Increasingly, the ambitions of non-

traditional players in the UK market are gaining credibility, with new

entrants active and seeking to build their platforms by acquiring

businesses made available through restructuring of incumbents. The

Group distributes life assurance products to banking customers in

competition with independent advisors and life assurance companies.

In the UK credit card market large retailers and specialist card issuers are

active in addition to the UK banks. In addition to physical distribution

channels, providers compete through direct marketing activity and the

internet.

In Wealth Management, The Royal Bank of Scotland International

competes with other UK and international banks to offer offshore banking

services. Coutts and Adam & Company compete as private banks with

UK clearing and private banks, and with international private banks.

Competition in wealth management remains strong as banks maintain

their focus on competing for affluent and high net worth customers.

In Ireland, Ulster Bank competes in retail and commercial banking with

the major Irish banks and building societies, and with other UK and

international banks and building societies active in the market. The

challenging conditions in the Irish economy persist and many of the

domestic Irish banks have required State support and are engaged in

significant restructuring actions.

In the United States, RBS Citizens competes in the New England, Mid-

Atlantic and Mid-West retail and mid-corporate banking markets with local

and regional banks and other financial institutions. The Group also

competes in the US in large corporate lending and specialised finance

markets, and in fixed-income trading and sales. Competition is principally

with the large US commercial and investment banks and international

banks active in the US. The economic recovery in the US is proving

weaker than expected and loan demand is weak in Citizens’ markets.